5-point checklist to help you identify the right tax-saving investments

- Sujit Bangar

- Jan 20, 2022

- 3 min read

5-point checklist to help you identify the right tax-saving investments

Remember, finance is personal. What works for someone else may not be the best thing for you.

To get the maximum value from your tax-saving investments, they must fit in your financial story and work towards meeting your financial goals. So, if you are confused about which tax-saving investment is best for you, worry not.

In this post, we share a 5-point checklist. This checklist will help you filter out from available tax-saving investment options & help select the right fit for your financial needs.

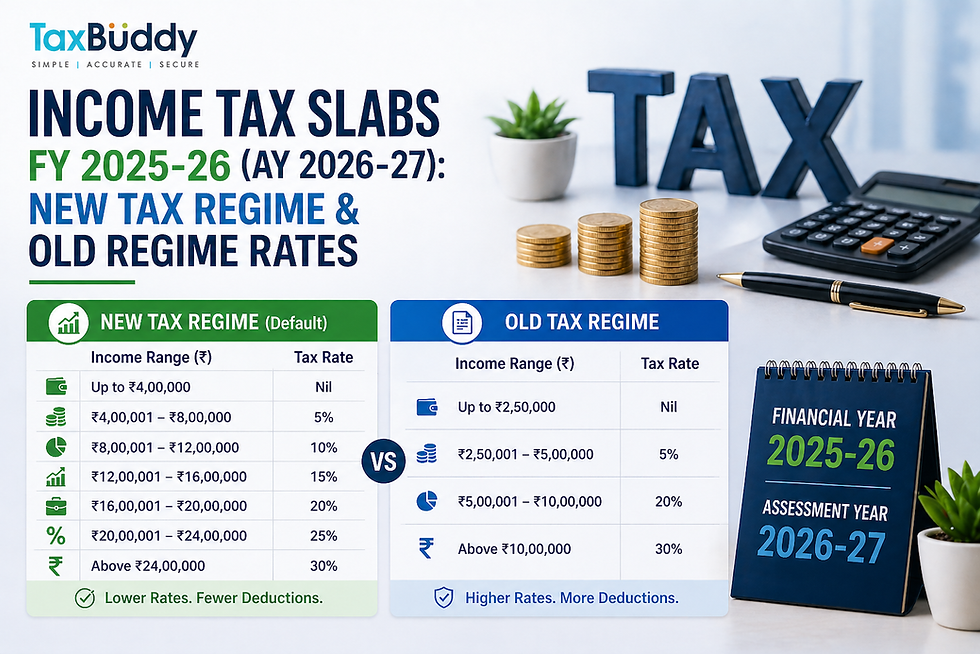

Check # 1: Old vs new tax regime

In Budget 2020, the Finance Minister made a significant change by introducing a new tax regime. The new tax regime consists of lower tax rates & minimal exemptions. As a young investor, you need to choose which regime you want to be covered in.

Suppose you choose to be covered in the old tax regime. In that case, you need to invest in the above tax-saving avenues to cover the entire limit (, e.g. INR 1.5 lacs for 80C and so on) to avail of the total tax benefit. If you choose to be governed by the new tax regime, you do not restrict yourself to conventional tax-saving investments like PPF, ELSS, NPS etc.

So, before proceeding forward, first, make an informed decision on which tax regime you want to cover yourself in. This will help you clarify the universe of investment products available to you & then you can make a better decision.

Check # 2: Your financial goals

The constant barrage of advertisements and sales pitches that you see daily sell you on either return or tax benefit. No-one speaks about the most important thing – your financial goals.

Remember, no investment is good or bad. It is only as good or bad as much as it helps to meet your financial goal.

So, first, prepare a list of your financial goals. This will include how much money you want & when you want. Once you are clear on this, you can take the correct decision on where to invest.

Ideally, given the lock-in period of most tax-saving investments, you can consider them only for goals more than 5 years away.

Goal | Time horizon | Suggested Investments |

Short term | Less than 5 years | Do not invest in tax-saving products because of the lock-in requirements & tax implications of early withdrawal. Instead, consider FD/ debt mutual funds. |

Medium Term | 5-10 years | ELSS, Tax Saving Bank FD, NSC |

Long term | > 10 years | ELSS, PPF |

Check # 3: Your risk tolerance & Asset Allocation

A good tax-saving investment should align with your risk tolerance. Simply put, risk tolerance is the percentage of total wealth invested in equity markets and still be able to sleep peacefully at night.

So, first, you should assess your risk tolerance and decide on a mix of investments. This is also known as asset allocation. For example, assume that your risk tolerance is 60:40 in equity & debt. You should have 60% into equity products at any given time.

When choosing a new tax-saving investment, you need to check your existing asset allocation. This will help you choose an investment that brings it in alignment with your ideal asset allocation.

For example, suppose your existing allocation in equity & debt is 30:70, and the ideal allocation is 60:40. In that case, you can purchase ELSS mutual funds. This will not save tax well as bring your asset allocation towards the ideal allocation.

Check # 4: Evaluate the tax impact across the investment’s life cycle

While selecting a tax-saving investment product, people make the mistake to only consider the immediate tax saving at the time of investment. However, as an informed investor, you should also carefully examine the tax impact across the life cycle of the product, which comprises the following:

COMPARATIVE LIFE CYCLE TAXATION OF COMMON TAX SAVING AVENUES

Stage | PPF | EPF | ELSS | NPS | ULIP | Tax Saving FD |

Investment | E | E | E | E | E | E |

Income | E | E (taxable if annual contribution > INR 2.5 lacs* | E (dividends are taxable) | E | E | T |

Maturity | E | E (subject to conditions) | E (LTCG above INR 1 lac taxable @10%) | E (annuities are fully taxable) | E (capital gains taxable @ 10% if annual premium > INR 2.5 lacs* | E |

(E – Exempt; T – Taxable) *As proposed in Budget 2021

Check # 5: Lock-In period of the investment:

Don’t be in a rush to blindly invest in a tax-saving investment without considering the lock-in period. There is not much wisdom in locking your money for some petty tax saving. And when the money is needed, taking an expensive personal loan.

Hence, it is essential that you clearly identify which goal you are investing this money before investing. Then check when the money is due, & ensure that the lock-in period of the proposed investment is less than the time to goal.

For example, if you plan to invest in your kid’s education 8 years away, investing in PPF won’t be a great idea as it has a 15-year lock-in period. Instead, you can consider ELSS mutual funds.

Conclusion

Tax saving is not an end in itself. It is just a piece of the entire financial puzzle. When you choose to invest in tax-saving investments that align with your financial goals & risk tolerance, you avoid costly investment mistakes. And you also increase your chances of achieving your financial goals in a hassle-free way.

Check out FINBINGO TAX PLANNER Now!

Comments