House Rent Allowance (HRA): Your Complete Guide to Exemption, Calculation & Rules (AY 2025-26)

- PRITI SIRDESHMUKH

- Jul 22, 2025

- 13 min read

House Rent Allowance (HRA) is a really important part of your salary if you live in a rented house because it can lead to significant tax savings. Many people look forward to HRA as it helps reduce their taxable income. This article will explain what House Rent Allowance (HRA) means, how you can calculate the HRA exemption, and what HRA rules you need to follow. It will also cover the documents you need and how TaxBuddy can assist you with this. This guide provides all the necessary details for the Assessment Year 2025-26, helping you with understanding your salary structure. Did you know that a proper HRA claim can noticeably increase your take-home pay?

Table of Content

What is House Rent Allowance (HRA) in Salary?

House Rent Allowance, or HRA, is money your employer gives you as part of your salary to help pay for your rented home. The HRA full form stands for House Rent Allowance. Its main purpose is to help employees cover their rental accommodation costs. The HRA in salary is a common component for salaried individuals. This allowance can be partly or sometimes even fully exempt from your taxes, but this depends on certain conditions mentioned in Section 10(13A) of the Income Tax Act. If you're an employee paying rent for your house, HRA is meant for you. The employer provides this benefit to the employee to ease the financial load of rent. Understanding HRA meaning helps in optimizing your salary structure for better tax benefits.

Who Can Claim HRA Exemption?

To claim HRA exemption, an employee must meet specific conditions. HRA eligibility is an important aspect for salaried individuals. You must be a salaried employee, and HRA must be a part of your Cost to Company (CTC) or salary package. Crucially, you must live in a rented accommodation and actually be paying rent for it. If you are not living in rented premises, for example, if you live in your own house, you cannot claim HRA exemption, and the entire HRA amount received becomes fully taxable. This HRA tax benefit is designed to help with the expense of renting a home.

Here are the key conditions for HRA exemption:

You must be a salaried individual.

HRA must be a component of your salary.

You must reside in a rented property.

You must be paying rent for the accommodation.

It’s a common question: "Can I claim HRA if I live in my own house?" The answer is no. HRA benefits are only for those who pay rent. Making sure you meet these criteria is the first step to successfully claiming deductions in your ITR.

How to Calculate HRA Exemption: The 3 Golden Rules (Section 10(13A))

The HRA calculation formula is central to understanding your tax savings. As per Section 10(13A) of the Income Tax Act, read with Rule 2A of the Income Tax Rules, the amount of HRA exemption you can claim is the minimum of the three amounts calculated using the HRA deduction rules. This HRA calculation involves your basic salary, dearness allowance (if it forms part of retirement benefits and is mentioned in the employment contract), the city you live in (metro or non-metro), and the actual rent you pay.

Condition 1: Actual HRA Received from Employer

Actual HRA received from your employer is the first amount to consider for HRA exemption. This is simply the total HRA component that your employer has paid to you during the financial year, as specified in your salary.

Condition 2: Rent Paid in Excess of 10% of Salary

Rent paid in excess of 10% of salary is the second condition in HRA calculation. You calculate this as: Actual Rent Paid - (10% of 'Salary for HRA'). 'Salary for HRA' here means your basic salary plus any Dearness Allowance (DA) that forms part of your retirement benefits, and any fixed commission.

Condition 3: 50% of Salary (Metro Cities) or 40% of Salary (Non-Metro Cities)

The third condition for HRA exemption depends on your city: it's 50% of your 'Salary for HRA' if you live in a metro city, or 40% of your 'Salary for HRA' if you live in a non-metro city. For HRA calculation, the designated metro cities are Delhi, Mumbai, Chennai, and Kolkata. For all other cities, the limit is 40%. You can Use our HRA Calculator to simplify this or check against official Income Tax Department guidelines.

HRA Calculation Examples (for AY 2025-26)

Seeing an HRA calculation example makes the rules much clearer. Let's look at a few HRA exemption examples to illustrate how to calculate HRA with different scenarios for Assessment Year 2025-26. We will assume Dearness Allowance (DA) forms part of retirement benefits for these examples.

Example 1: Salaried individual in Mumbai (Metro City) Suppose Priya works in Mumbai.

Her Basic Salary is ₹60,000 per month.

Dearness Allowance (DA) is ₹10,000 per month (forms part of retirement benefits).

Actual HRA received is ₹30,000 per month.

Actual rent paid is ₹25,000 per month.

First, calculate annual figures:

Salary for HRA = (Basic + DA) 12 = (₹60,000 + ₹10,000) 12 = ₹70,000 * 12 = ₹8,40,000.

Actual HRA received = ₹30,000 * 12 = ₹3,60,000.

Actual rent paid = ₹25,000 * 12 = ₹3,00,000.

Now, apply the three conditions:

Actual HRA received: ₹3,60,000.

Rent paid in excess of 10% of salary: ₹3,00,000 - (10% of ₹8,40,000) = ₹3,00,000 - ₹84,000 = ₹2,16,000.

50% of salary (since Mumbai is a metro city): 50% of ₹8,40,000 = ₹4,20,000.

The minimum of these three amounts is ₹2,16,000. So, Priya's HRA exemption is ₹2,16,000. The taxable HRA will be ₹3,60,000 (Actual HRA) - ₹2,16,000 (Exempt HRA) = ₹1,44,000.

Example 2: Salaried individual in Pune (Non-Metro City) Let's say Rohan works in Pune.

His Basic Salary is ₹40,000 per month.

Dearness Allowance (DA) is ₹5,000 per month (forms part of retirement benefits).

Actual HRA received is ₹15,000 per month.

Actual rent paid is ₹12,000 per month.

Annual figures:

Salary for HRA = (₹40,000 + ₹5,000) 12 = ₹45,000 12 = ₹5,40,000.

Actual HRA received = ₹15,000 * 12 = ₹1,80,000.

Actual rent paid = ₹12,000 * 12 = ₹1,44,000.

The three conditions for HRA calculation:

Actual HRA received: ₹1,80,000.

Rent paid in excess of 10% of salary: ₹1,44,000 - (10% of ₹5,40,000) = ₹1,44,000 - ₹54,000 = ₹90,000.

40% of salary (since Pune is a non-metro city): 40% of ₹5,40,000 = ₹2,16,000.

The minimum of these three is ₹90,000. Rohan's HRA exemption is ₹90,000. Taxable HRA = ₹1,80,000 - ₹90,000 = ₹90,000.

Example 3: Scenario where actual HRA received is the lowest Consider Anjali who works in Hyderabad (Non-Metro).

Basic Salary: ₹30,000 per month.

DA (forms part of retirement): ₹3,000 per month.

Actual HRA received: ₹8,000 per month.

Actual rent paid: ₹10,000 per month.

Annual figures:

Salary for HRA = (₹30,000 + ₹3,000) 12 = ₹33,000 12 = ₹3,96,000.

Actual HRA received = ₹8,000 * 12 = ₹96,000.

Actual rent paid = ₹10,000 * 12 = ₹1,20,000.

HRA calculation conditions:

Actual HRA received: ₹96,000.

Rent paid in excess of 10% of salary: ₹1,20,000 - (10% of ₹3,96,000) = ₹1,20,000 - ₹39,600 = ₹80,400.

40% of salary (Non-metro): 40% of ₹3,96,000 = ₹1,58,400.

In this case, the lowest amount is ₹80,400 (Rent paid minus 10% of salary). Let's adjust the example slightly to make actual HRA received the lowest. Imagine Anjali's HRA received is only ₹5,000 per month, so ₹60,000 annually.

Actual HRA received: ₹60,000.

Rent paid in excess of 10% of salary: ₹80,400.

40% of salary (Non-metro): ₹1,58,400.

Now, the actual HRA received (₹60,000) is the lowest. So, Anjali's HRA exemption is ₹60,000. Taxable HRA = ₹60,000 - ₹60,000 = ₹0.

Try Our Easy HRA Exemption Calculator!

Figuring out your HRA exemption can seem a bit tricky with all the rules. Our HRA calculator online simplifies this entire process for you. Just enter your salary details, HRA received, and rent paid, and this online tool will instantly show your eligible tax exemption. It's a free HRA calculator designed to be user-friendly and accurate, "Powered by TaxBuddy". Why not Calculate Your HRA Exemption Now and see how much you can save?

Documents Required to Claim HRA Exemption

To successfully claim HRA exemption, you need proper documents for HRA claim. The primary HRA proof is your rent receipts. You also need a rental agreement, especially for a substantial claim. If your annual rent payment exceeds ₹1,00,000 (which is ₹8,333 per month), you must provide your landlord's PAN to your employer. If the landlord does not have a PAN, they must give you a declaration to this effect (sometimes along with Form 60). You should also submit Form 12BB to your employer, which is a declaration of your investments and expenses eligible for tax deductions, including HRA.

Here’s a checklist of documents:

Rent receipts (monthly or quarterly).

Rental agreement (preferably stamped).

Landlord's PAN card copy (if annual rent is over ₹1,00,000).

Declaration from landlord if PAN is not available.

Duly filled Form 12BB.

Important: Keep these documents safe for future reference, as the tax department might ask for them later. You can Learn more about Form 12BB.

How to Claim HRA Exemption: Step-by-Step

You can claim your HRA exemption in two main ways. The HRA declaration to employer is the most common method, but you can also claim HRA in ITR if you miss that. This process helps reduce your taxable salary.

Claiming HRA through Your Employer

Claiming HRA through your employer is straightforward. You need to submit the required documents like rent receipts, the rental agreement, and Form 12BB to your HR or payroll department. They usually ask for these proofs towards the end of the financial year, typically between January and March. Ensure timely submission to your employer. This allows them to calculate your HRA exemption correctly and adjust your Tax Deducted at Source (TDS), which will then be reflected in your Form 16.

Claiming HRA while Filing Your Income Tax Return (ITR)

If you somehow missed submitting the HRA proofs to your employer, or if your employer didn't consider it, you can still claim HRA while filing your Income Tax Return (ITR). When you file your ITR, you'll need to calculate the exempt HRA amount yourself and then deduct it from your gross salary to arrive at your taxable salary. You should report the exempt HRA under the 'allowances to the extent exempt u/s 10' in the ITR form. Even if you claim it directly in your ITR, it's very important to keep all the proofs like rent receipts and the rental agreement safe. The tax department can ask for these documents later during an assessment. TaxBuddy can help you File your ITR with TaxBuddy accurately.

HRA and the New Tax Regime vs. Old Tax Regime

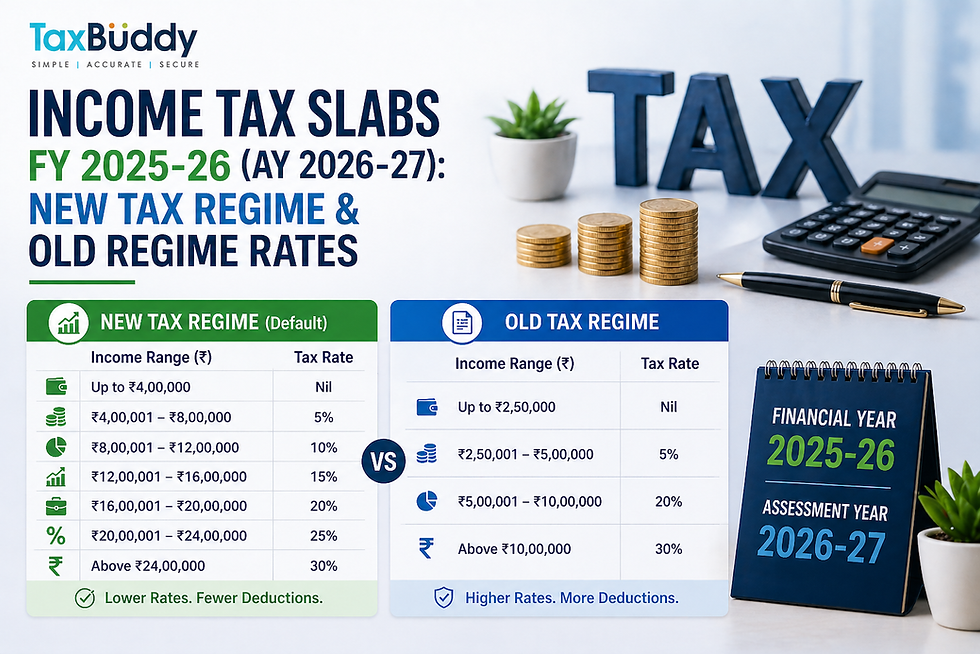

Understanding HRA new tax regime versus HRA old tax regime rules is crucial for your tax planning. The HRA exemption is available if you opt for the Old Tax Regime. However, if you choose the New Tax Regime (under Section 115BAC of the Income Tax Act), you generally cannot claim HRA exemption. The new regime offers lower tax rates but disallows most common deductions and exemptions, including HRA. So, it's an important consideration for tax planning. You need to evaluate whether the benefit of lower tax rates in the new regime outweighs the HRA exemption and other deductions available in the old regime. This choice will significantly impact your final tax liability. .

Special Scenarios for HRA Claim

There are several special scenarios for HRA claims that people often ask about. It's good to know how HRA rules apply when you are, for instance, HRA living with parents or claiming HRA and home loan benefits together.

Can I Claim HRA if I Live with My Parents?

Yes, you can claim HRA if you live with your parents and pay them rent. For this HRA claim to be valid, you must have a formal rental agreement with your parents. You should transfer the rent amount to their bank account regularly. Also, your parents must show this rent as rental income in their own income tax returns. This makes the transaction legitimate.

Can I Claim HRA if I Pay Rent to My Spouse?

Claiming HRA if I pay rent to my spouse is generally not advisable. The Income Tax department often views such transactions with skepticism and may consider them a sham transaction designed solely to avoid tax, unless it is a genuinely commercial arrangement. It's hard to prove that the arrangement isn't just a way to divert income. So, it's best to avoid this to prevent future tax issues.

Claiming HRA and Home Loan Benefits Simultaneously

Yes, you can claim HRA and home loan benefits (like interest deduction under Section 24 and principal repayment under Section 80C) simultaneously. This is possible if you own a house (for which you have a home loan) in one city, but you live in a rented house in a different city for your employment. It can also apply if your owned house is let out, or if your family lives in your owned house while you work and rent in another city. You should have genuine reasons and proper documentation for both. Knowing about tax benefits on home loans is also helpful here.

What if My Landlord Doesn't Have a PAN?

If your annual rent payment exceeds ₹1,00,000, providing your landlord's PAN is mandatory for your HRA claim with the employer. If the landlord doesn't have a PAN, they must provide you with a declaration stating this, and sometimes they might also need to fill out Form 60. If your landlord doesn't provide either their PAN or the declaration, your HRA claim might face problems, or your employer might not allow the full exemption.

HRA for Work From Home (WFH) Scenarios

HRA for Work From Home (WFH) scenarios can be claimed. If you are genuinely paying rent for an accommodation from where you are working, even if it's in your hometown, you can claim HRA subject to all other standard conditions. The key requirements are that you are actually paying rent and have a valid rental agreement in place. The location being your work-from-home base doesn't automatically disqualify the HRA claim, as long as it's a legitimate rental arrangement.

What if You Don't Receive HRA but Pay Rent?

If you pay rent but don't receive HRA from your employer, you might still get a tax benefit using the Section 80GG deduction. This provision is for individuals, whether salaried or self-employed, who pay for rented accommodation but don't get any House Rent Allowance. To claim this deduction, you (or your spouse or minor child) should not own any residential accommodation at the place where you currently reside, perform duties of office, or employment or carry on business or profession. You will also need to file Form 10BA declaring that you meet the conditions.

The amount of deduction available under Section 80GG is the least of the following:

₹5,000 per month (₹60,000 annually).

25% of your adjusted total income.

Actual rent paid minus 10% of your adjusted total income.

Adjusted total income for this purpose means your gross total income less long-term capital gains, short-term capital gains under section 111A, and deductions under sections 80C to 80U (except Section 80GG). This is a useful provision for freelancers, consultants, or employees without an HRA component in their salary and helps them with other tax deductions.

Common Mistakes to Avoid When Claiming HRA

People often make HRA mistakes when claiming their exemption. Avoiding common HRA errors can save you from future tax notices and potential penalties.

Here are some frequent missteps:

Not having valid rent receipts or a rental agreement: These are crucial proofs.

Incorrectly calculating 'salary' for HRA: Remember to include basic pay and qualifying DA.

Claiming HRA when not living in a rented property: This is not allowed and can lead to issues.

Not providing the landlord's PAN when the annual rent exceeds ₹1,00,000: This is a mandatory requirement.

Claiming HRA under the new tax regime without checking the rules: HRA is generally not available under the new regime by default.

Submitting fake rent receipts: This can lead to severe penalties and scrutiny from the tax department.

Being careful and engaging in effective tax planning can help you steer clear of these HRA issues.

Conclusion: Maximize Your Tax Savings with Correct HRA Claims

To sum it up, HRA is a very valuable part of your salary that provides a great HRA tax saving opportunity. Understanding the HRA rules for calculation and ensuring you have all the necessary documentation is vital for maximizing this HRA benefit. The choice between the old and new tax regimes also significantly impacts your HRA exemption eligibility. It’s important to make correct HRA claims to avoid any issues later. For accurate HRA claims and overall tax planning, feel free to use TaxBuddy's resources, like our HRA calculator, or Get Expert Tax Advice from TaxBuddy.

Frequently Asked Questions (FAQs) about HRA

1. What is the full form of HRA?

Answer: HRA stands for House Rent Allowance.

2. Is HRA fully taxable?

Answer: HRA is partially taxable. The exemption is calculated based on a few factors like the rent paid, the salary, and the place of residence. The balance after exemption is taxable.

3. Can I claim HRA if I change jobs during the year?

Answer: Yes, you can claim HRA for the period you received it, provided you meet the eligibility criteria and submit rent receipts for that period.

4. What if my rent changes mid-year? How does it affect HRA?

Answer: If your rent changes mid-year, the HRA exemption will be recalculated based on the new rent amount for the remaining months of the year.

5. Is HRA exemption calculated monthly or annually?

Answer: HRA exemption is calculated monthly but is considered as part of your total salary for the year.

6. My landlord is an NRI. Can I still claim HRA?

Answer: Yes, you can still claim HRA if your landlord is an NRI. However, TDS implications may arise on the rent payment, and you may need to deduct TDS under Section 195.

7. Do I need stamped rent receipts?

Answer: Stamped rent receipts are not mandatory, but they are recommended, especially for larger amounts or if there is no formal rental agreement.

8. What if I pay rent for only a few months in a year?

Answer: You can claim HRA for the months you actually paid rent. The exemption will be calculated based on the rent paid during that period.

9. Can I claim HRA and 80GG both?

Answer: No, you cannot claim both HRA and 80GG for the same period. 80GG can be claimed only if you are not receiving HRA.

10. What is Form 12BB and is it mandatory for HRA?

Answer: Form 12BB is a declaration form where you can claim deductions, including HRA. It is mandatory for salaried individuals to submit this form to claim HRA.

11. Can HRA be claimed if I move to a new city for work?

Answer: Yes, you can claim HRA if you move to a new city for work, provided you meet all the eligibility conditions and pay rent.

12. What happens if I don't submit HRA proofs to my employer?

Answer: If you don't submit the necessary HRA proofs (like rent receipts or the landlord’s PAN), your employer may not grant HRA exemption, and the full HRA amount will be taxable.

13. Does HRA include maintenance charges paid to the society?

Answer: Generally no, unless the rent and maintenance charges are part of a composite rent agreement.

14. How is HRA shown in Form 16?

Answer: HRA exemption is usually shown as part of the total salary in Form 16, specifically under the section for exemptions.

15. Is there a maximum limit on the rent I can pay to claim HRA?

Answer: There is no direct limit on rent, but the exemption is capped based on your salary, the rent paid, and the place of residence. The exemption is calculated using a formula that considers these factors.

Comments