Section 80C Deductions for PPF, EPF, and Other Investments: How to Report in Your ITR

- Dipali Waghmode

- Jul 1, 2025

- 9 min read

Section 80C of the Income Tax Act offers one of the most widely used avenues for taxpayers to reduce their taxable income and, consequently, their overall tax liability. This section allows for a deduction of up to ₹1.5 lakh annually on eligible investments, making it a significant benefit for tax-saving purposes. Many popular tax-saving instruments fall under Section 80C, such as the Public Provident Fund (PPF), Employee Provident Fund (EPF), National Savings Certificates (NSC), and more. The investments under this section help individuals save for the future while also reducing their tax burden.

Lets delve into the investments that qualify for deductions under Section 80C, how to report these deductions when filing your Income Tax Return (ITR), and common mistakes that taxpayers should avoid. Additionally, we’ll discuss the latest updates for AY 2025–26 that impact Section 80C deductions.

Table of Contents

What Investments Qualify Under Section 80C?

Section 80C covers a broad range of investments and expenses that allow taxpayers to reduce their taxable income. Here are some of the most common investments that qualify for this deduction:

Public Provident Fund (PPF): PPF is one of the most popular and safest investment options, offering tax-free returns and a lock-in period of 15 years. Contributions to PPF are eligible for deductions under Section 80C, and the interest earned is exempt from tax.

Employee Provident Fund (EPF): EPF is a retirement savings scheme for salaried employees. Contributions made by both the employer and the employee are eligible for tax deductions under Section 80C, and the accumulated corpus is tax-free at the time of withdrawal, subject to certain conditions.

National Savings Certificates (NSC): NSC is a fixed-income investment scheme offered by India Post. It has a 5-year maturity period, and the investment is eligible for tax deductions under Section 80C. Additionally, the interest earned on NSCs is taxable, but it can be claimed as a deduction during the tenure of the certificate.

National Pension Scheme (NPS): NPS allows for retirement savings and offers tax benefits under both Section 80C and an additional section (Section 80CCD). Contributions to NPS are eligible for a tax deduction, making it a popular choice for long-term savings.

Tax-saving Fixed Deposits: Tax-saving fixed deposits with a minimum lock-in period of 5 years also qualify for deductions under Section 80C. These deposits offer fixed returns, and the interest earned is subject to tax.

Life Insurance Premiums: Premiums paid for life insurance policies for yourself, your spouse, children, or Hindu Undivided Family (HUF) members are eligible for tax deductions under Section 80C.

Home Loan Repayment (Principal): The principal repayment of a home loan is also eligible for deduction under Section 80C, up to ₹1.5 lakh per year. However, the interest on the loan is claimed separately under Section 24(b).

Children’s Tuition Fees: Tuition fees paid for the education of children in India qualify for deductions under Section 80C. However, this is restricted to a maximum of two children.

PPF, EPF, and Other Key Investments Explained

Public Provident Fund (PPF): PPF is a government-backed scheme offering tax-free returns. It provides an interest rate that is generally higher than savings accounts, and the interest is compounded annually. PPF contributions are locked in for 15 years, which can be extended in blocks of 5 years. The principal and interest earned are exempt from tax. This makes PPF a highly favored option for long-term retirement planning and tax-saving.

Employee Provident Fund (EPF): EPF is mandatory for salaried employees earning below a specific threshold. Both employee and employer contribute to the fund, with the employee’s contribution being eligible for a deduction under Section 80C. The accumulated balance earns interest, and withdrawals are exempt from tax if made after a certain period (usually 5 years).

National Savings Certificates (NSC): NSC is a 5-year investment with a fixed interest rate, issued by India Post. The principal invested in NSC qualifies for tax deduction under Section 80C. Interest earned on NSC is taxable, but it can be claimed as a deduction during the tenure of the certificate. It is ideal for conservative investors who seek a fixed, secure return.

National Pension Scheme (NPS): NPS is a government-backed scheme aimed at retirement planning, where you can invest in a mix of equity, corporate bonds, and government securities. Contributions to NPS are eligible for tax deductions under both Section 80C and Section 80CCD. The government also offers an additional ₹50,000 deduction under Section 80CCD(1B), making NPS a powerful tool for retirement savings.

Tax-saving Fixed Deposits: These are fixed deposits with a 5-year lock-in period, offered by various banks. The principal invested in these fixed deposits qualifies for tax deductions under Section 80C, though the interest earned is taxable.

How to Report Section 80C Deductions in Your ITR

When filing your Income Tax Return (ITR), you must report the deductions claimed under Section 80C correctly to ensure that your tax liability is accurately calculated. Here’s a step-by-step guide on how to report Section 80C deductions in your ITR:

Identify the Eligible Investments: Collect all the details of your investments and expenses eligible under Section 80C, such as PPF contributions, EPF, NSC, life insurance premiums, and home loan principal repayments.

Use the Correct ITR Form: Depending on your income sources, choose the appropriate ITR form. Individuals with income from salary, house property, or other sources typically use ITR-1 (Sahaj) or ITR-2. Ensure the correct form is selected to report your deductions under Section 80C.

Report the Total Deduction: In the ITR form, there is a specific section for deductions under Chapter VI-A. Enter the total amount you have invested in eligible instruments under Section 80C. The amount must not exceed ₹1.5 lakh in total for the financial year.

Provide Investment Details: Depending on the specific instrument, you may need to provide additional information, such as policy numbers for life insurance, account numbers for PPF, or the loan account number for home loan principal repayment.

Claim the Deduction: After entering the relevant details, the ITR software will automatically calculate your taxable income after applying the deduction under Section 80C. Ensure all amounts are correctly reported to avoid discrepancies.

Common Mistakes to Avoid

While claiming deductions under Section 80C is beneficial, taxpayers often make some common mistakes. Here are some of the key mistakes to avoid:

Exceeding the Limit: The maximum deduction available under Section 80C is ₹1.5 lakh. Any amount exceeding this limit will not be eligible for deductions, so ensure that your total investments do not exceed this limit.

Incorrect Reporting: Ensure all investments and premiums are correctly reported in the ITR. Failure to mention specific details, such as policy numbers or account numbers, can lead to the rejection of the deduction.

Ignoring the Lock-In Periods: Some investments like tax-saving fixed deposits or PPF have lock-in periods. Make sure you understand the lock-in rules, as early withdrawals may affect your eligibility for tax benefits.

Misunderstanding of Eligible Expenses: Many taxpayers incorrectly claim expenses that do not qualify under Section 80C, such as rent or daily living expenses. Only specific investments and payments qualify, so be careful.

Latest Updates for AY 2025–26

For the Assessment Year 2025-26, there are no major changes to Section 80C. However, it is important to note that the government may revise the available interest rates for schemes like PPF, NSC, or tax-saving fixed deposits. Additionally, new schemes or instruments could be introduced that qualify for deductions under Section 80C. Therefore, it is always advisable to stay updated with the latest announcements by the CBDT to maximize your tax-saving opportunities.

Conclusion

Claiming Section 80C deductions is essential for effective tax planning, but accurate reporting is equally critical to avoid tax notices and penalties. Platforms like TaxBuddy simplify this process by:

Auto-filling ITR forms using Form 16 and other data

Suggesting eligible deductions based on your profile

Cross-verifying entries with Form 26AS and AIS

Providing expert support if you receive a tax notice or need help responding

For anyone looking for assistance in tax filing, it is highly recommended to download theTaxBuddy mobile app for a simplified, secure, and hassle-free experience.

FAQs

Q1. Does TaxBuddy offer both self-filing and expert-assisted plans for ITR filing, or only expert-assisted options?

Yes, TaxBuddy provides both self-filing and expert-assisted plans. The self-filing option is designed for taxpayers who are comfortable navigating the process on their own, offering tools and guidance for smooth filing. On the other hand, the expert-assisted plan is perfect for individuals or businesses who prefer professional help to ensure compliance and accuracy. This dual approach allows taxpayers to choose based on their level of experience and comfort with tax filing.

Q2. Which is the best site to file ITR?

TaxBuddy is widely regarded as one of the most reliable and user-friendly platforms for filing ITR. It provides a comprehensive solution that simplifies the filing process, ensuring that even complex returns are filed with ease. The platform offers expert assistance, real-time error checking, and seamless integration, making it an excellent choice for both beginners and seasoned taxpayers. While the official Income Tax Department website is also an option, TaxBuddy's user-centric design and additional support make it a strong contender for the best site to file ITR.

Q3. Where to file an income tax return?

You can file your ITR on the official Income Tax Department website or through trusted tax filing platforms like TaxBuddy. Filing through the Income Tax Department portal is a reliable method, but for a simplified experience, platforms like TaxBuddy offer a more user-friendly interface, error-checking, and personalized assistance, making it easier for taxpayers to comply with the tax filing process.

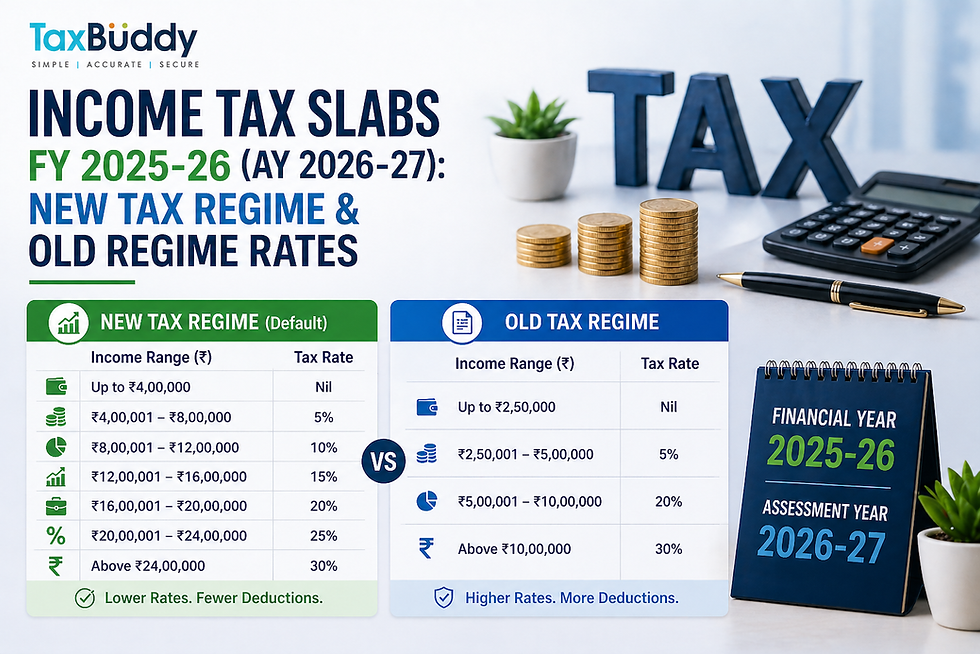

Q4. Can I claim Section 80C deduction if I opt for the new tax regime?

No, taxpayers who opt for the new tax regime under Section 115BAC cannot claim deductions under Section 80C. The new tax regime offers lower tax rates but eliminates most exemptions and deductions. Therefore, if you wish to avail of Section 80C deductions, you must choose the old tax regime, where these deductions and exemptions are applicable.

Q5. What is the maximum limit for Section 80C deduction?

The maximum limit for Section 80C deductions is ₹1.5 lakh per financial year. This limit includes various eligible investments and expenses such as life insurance premiums, PPF contributions, EPF, tax-saving fixed deposits, and tuition fees for children. It is essential to keep track of your investments to maximize the benefit under this section.

Q6. Do I need to submit proof of investment with my ITR?

No, you are not required to submit proof of investment while filing your ITR. However, it is crucial to retain all supporting documents, such as receipts or statements, for at least six years. These documents may be requested for verification by the Income Tax Department in case of a tax audit or inquiry.

Q7. How do I report PPF and EPF contributions in my ITR?

Both Public Provident Fund (PPF) and Employees’ Provident Fund (EPF) contributions are eligible for deductions under Section 80C. You need to disclose the contributions in the “Deductions” section of your ITR form, specifying the amount contributed and the respective payee details. Make sure the total contribution does not exceed the ₹1.5 lakh limit under Section 80C.

Q8. What should I do if I get a tax notice for incorrect 80C reporting?

If you receive a tax notice regarding incorrect Section 80C reporting, the first step is to review the notice carefully. Verify the deductions and cross-check them with your documents. If there is a discrepancy, gather the supporting documents and respond to the notice through the e-filing portal. TaxBuddy can assist you in handling the notice and filing any necessary corrections or revised returns.

Q9. Is it necessary to cross-check the deductions with Form 26AS?

Yes, it is essential to cross-check the deductions claimed with the details in Form 26AS to ensure they match the records provided by your employer and the Income Tax Department. Form 26AS contains a summary of all the taxes deducted and deposited against your PAN, including TDS credits, which must be correctly reflected in your ITR to avoid any discrepancies.

Q10. Can I claim deductions for EPF contributions made by my employer?

No, you cannot claim deductions for EPF contributions made by your employer under Section 80C. Only the employee’s own contributions to the EPF are eligible for deduction under this section. Employer contributions are considered part of your salary and are not eligible for additional deductions.

Q11. Are there any changes in the ITR forms for AY 2025-26?

Yes, there are several changes in the ITR forms for Assessment Year (AY) 2025-26. One significant change is the mandatory detailed disclosure of each 80C investment. Taxpayers will need to list individual investments such as PPF, EPF, life insurance premiums, and other eligible expenses, along with the corresponding amounts and details. This update aims to improve transparency and streamline the filing process.

Q12. Can I claim deductions for both life insurance premiums and EPF contributions?

Yes, you can claim deductions for both life insurance premiums and EPF contributions under Section 80C, as long as they meet the eligibility criteria. Life insurance premiums paid for policies in your name, your spouse’s, or your children’s name are eligible, while contributions to the EPF are also deductible. However, the total deductions under Section 80C, including all eligible investments, must not exceed ₹1.5 lakh.

Comments