Special Allowance: A Detailed Guide for Taxpayers

- Farheen Mukadam

- Jul 9, 2024

- 6 min read

An amount of money given to employees by an organisation for a variety of purposes is known as a special allowance. All types of business entities, including sole proprietorships and major companies, have this provision requiring an additional contribution in an amount predetermined and fixed.

These benefits are exclusively determined by the base pay of the employee. Any such payment given above and above an employee's salary may be subject to taxation, with some exemptions depending on the purpose of the allowance. Like LTA and HRA, special allowances are subject to significant fluctuations based on a number of factors, including the employee's position and performance, the organization's financial standing, and the presence of employee benefit plans. In this detailed guide, we will highlight the tax treatment of special allowances.

Table of Contents

What is a Special Allowance?

An allowance is a set amount of money in addition to the salary that businesses provide their employees on a regular basis to fulfil specified needs. Unless otherwise exempt, all allowances are typically counted towards an employee's total income. The allowances are taxable in accordance with the rules established by the Income Tax Act and are in excess of the base wage.

The extra allowances offered by different companies vary greatly. Certain employers merely provide them as a "bonus" to express gratitude for an employee's outstanding work product. Conversely, other companies may offer a set compensation depending on the idea of "profit employment." The latter is explained quite well by the Income Tax Act of 1962. The amount of an allowance given to recognise extraordinary achievement is typically tax-free up to the total amount of incurred costs. Some employers provide their salary slips with a special allowance. The amount left over is recognised as a distinct allowance once all current overheads have been subtracted, including LTA, HRA, conveyance and dearness allowances, and so on.

According to Section 17(2) of the IT Act, 1961, any such stipend or advance that is set aside by an employer and paid for a particular expense is free from income tax. But this amount needs to be paid during the employee's employment while they are actively performing their assigned tasks. It also serves as an example of how an allowance and a perquisite differ from one another.

A corporation may offer increased pay, stock options, and other benefits to its top performers. If the employer or the corporation so chooses, it can also set up a that keeps their valued workers' living standards intact.

There is no income tax imposed on the paid allowances in either of these cases.

Illustrations

Example 1: Let us consider the following scenario: X works for company ABC. She discovers that she is entitled to a conveyance allowance of Rs. 1,500 per month when she examines her salary slip. This reimbursement is meant to cover the costs associated with travelling from one's home to one's place of employment. According to the Income Tax Act, there is no exemption for this allowance, and it is completely taxed.

Example 2: Y is employed by a school to carry out research, and she is entitled to a research stipend for the costs expended.

Example 3: Z is a public health physician assigned to a medical camp located in a rural area. This area is home to tribes. Z receives a tribal area allowance in addition to his base pay.

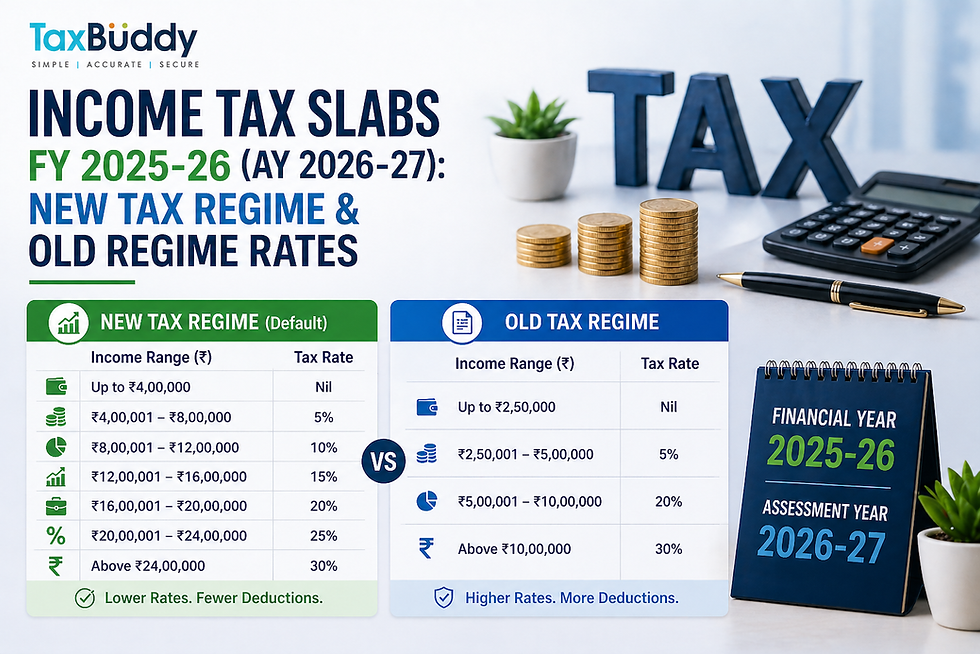

Exemptions for Special Allowance: Old & New Tax Regime

Tax Treatment for Special Allowance

The only grants or allowances that are taxable are those that aren't specifically covered by any IT Act exclusions. The IT Act of 1961's Section 10(14) governs the majority of exemptions. Additionally, extraordinary allowances are not taxable under certain circumstances; they are outlined in the IT sections that follow. They are:

Only if an allowance is not a requirement would exemptions apply. It is a crucial distinction that is only given to regular staff members.

The only advances that qualify for this exemption are those that are paid solely and exclusively for exceeding expectations at work and holding a profitable position.

Unusual payments made for personal or unique purposes are not exempt from taxes.

Lastly, the law does not set a maximum amount for an allowance.

Additionally, a few tax regulations relate to the following situations:

Any advances or payments made to the Supreme Court's Honourable Justices and the HCs may not be subject to taxes.

A corporation may be eligible for a partial tax exemption under Section 10(13A) if it additionally contains HRA.

There is never a tax exemption on any other stipend, such as the city compensatory allowance. Since different cities have differing cost of living, the laws governing Dearness Allowance, or DA, automatically apply in the last caveat.

Conclusion

A special allowance is typically assumed to be a component of variable income. You should be aware, though, that a special allowance is included in the gross salary. Furthermore, the policies of the organisation determine how a special allowance is allocated. Consequently, just because "Company A" gives a specific allowance to every employee, it does not follow that "Company B" has to do the same for every employee. You must add up the amounts listed under each eligible allowance head from the above list that applies to you to find the total amount you have received under the special allowance component of your income. See your pay stub for further information regarding the amount allotted to the special allowance.

FAQ

Q1. What is a special allowance in salary?

A special allowance is a sum of money given to employees to help with costs related to their work-related expenses. It is a set sum that is different for every company and usually mentioned in the offer letter and pay stub of a new hire. This allowance is meant to cover costs for things like meals, travel, and equipment that are specific to the employee's job.

Q2. Is Special allowance part of CTC?

Yes, your CTC will include all exceptional allowances. CTC stands for the cost to the business. It covers all costs incurred in relation to the staff.

Q3. Can I claim an exemption on special allowance under the new tax regime?

Under the current system, the majority of special allowance exemptions have been eliminated. Under the new tax system, exemptions like the LTA, HRA, and Section 10(14) exemptions get eliminated. There are, however, a few exceptions possible under section 10, such as gratuities, encashment of leave, and voluntary retirement.

Q4. Can a special allowance be more than the basic salary?

Your special allowance cannot exceed your base wage in accordance with the New Wage code 2022. For example, the base pay ought to represent at least 50% of the gross.

Q5. How is special allowance computed in salary slips?

Money that does not fall under any other head on a salary slip or the residual factor is regarded a special allowance. The amount that remains after deducting all other components of a pay slip, such as benefits, constitutes a special allowance. This amount represents the yearly CTC.

Q6. Is a special allowance in salary taxable or not?

Unless certain exclusions apply, the employee who receives an allowance is responsible for paying taxes on it. Sections 10(14)(i) and 10(14)(ii) of the Income Tax Act list certain extraordinary allowance exemptions.

Q7. What is a supplementary allowance?

One perk that an employee receives from their employer is a supplemental allowance. The supplementary allowance, also known as the special allowance, is the amount that remains after deducting the base wage, HRA, medical allowances, and transportation costs from your gross compensation.

Q8. What is the uniform allowance exemption limit for AY 2023-24?

According to Income Tax Act Section 10 (14) (ii), the entire cost of buying uniforms for official use is deductible. In this instance, there is no maximum restriction.

Q9. Can special allowances be exempted from tax?

Some special allowances can be exempted from tax if they are provided for specific purposes such as travel, research, or other professional expenses. The exemptions are subject to conditions laid down by tax laws.

Q10. How should special allowances be declared in the tax return?

Special allowances should be included in the total salary income and declared accordingly in the income tax return. If any part of the special allowance is exempt, it should be shown separately under the exempt income section.

Q11. How do special allowances impact an employee's take-home pay?

Special allowances can significantly impact an employee’s take-home pay by providing additional income beyond the basic salary. However, since many special allowances are taxable, the net effect on take-home pay will depend on the applicable tax rates and any possible exemptions.

Q12. Are there any industry-specific special allowances that employees should be aware of?

Yes, certain industries offer special allowances tailored to their specific needs. For example, the IT sector might offer a technology allowance, while the education sector might provide a research allowance. Understanding these can help employees maximize their benefits.

Comments