Income Tax Slabs FY 2025-26 (AY 2026-27): New Tax Regime & Old Regime Rates

- Ankita Murkute

- Apr 29

- 14 min read

Income tax slabs define the rate at which an individual’s income is taxed in India. For the financial year 2025-26, taxpayers have the option to choose between two tax regimes: the new tax regime and the old tax regime. Each regime follows a different approach to taxation, which directly affects the final tax payable.

The new tax regime continues as the default system. It offers lower tax rates across income levels but removes most exemptions and deductions that were traditionally used to reduce taxable income. In contrast, the old tax regime retains higher tax rates but allows taxpayers to claim a wide range of deductions, including those related to investments, insurance, housing, and salary components.

Table of Contents

Income Tax Slabs FY 2025-26 Overview

Income tax slabs refer to the classification of income into different ranges, where each range is taxed at a specific rate. As income increases, higher portions of income are taxed at progressively higher rates. This system ensures that taxation is applied in a structured and gradual manner rather than at a single flat rate.

For the financial year 2025-26, income tax in India is calculated under two separate frameworks. The new tax regime applies by default unless the taxpayer opts for the old tax regime. Both regimes use slab-based taxation, but they differ significantly in terms of rates, deductions, and overall tax calculation.

Under the new tax regime, the slab structure is designed to offer lower tax rates with minimal adjustments to income. Most exemptions and deductions are not available, which simplifies tax computation and reduces documentation requirements. This approach is aimed at making tax filing easier and more straightforward.

Under the old tax regime, the slab rates are higher, but taxpayers can reduce their taxable income by claiming various deductions and exemptions. These may include investment-based deductions, insurance premiums, housing-related expenses, and salary allowances. This system supports tax planning but requires proper tracking and reporting of eligible expenses.

Understanding how these two systems apply to your income is essential before making a choice. The difference in tax liability under each regime can vary depending on income level and the extent of deductions available.

What Is the New Tax Regime

The new tax regime is a simplified method of calculating income tax introduced to reduce the complexity of tax compliance. It follows a structure where tax rates are lower across different income slabs, but most exemptions and deductions are not available. This approach is designed to make tax calculation more straightforward and reduce the need for extensive tax planning.

Under this system, the focus shifts from claiming deductions to paying tax at concessional rates. The regime is now the default option for individuals and Hindu Undivided Families. Taxpayers are automatically placed under this regime unless they actively choose the old tax system while filing their return.

One of the key features of the new tax regime is the limited availability of deductions. Common deductions related to investments, insurance premiums, and housing loans are generally not allowed. However, certain benefits, such as the standard deduction for salaried individuals and specific employer contributions, may still be available, depending on the applicable rules.

Another important aspect is the rebate mechanism, which ensures that individuals with income up to a specified limit do not have to pay any tax. This effectively increases the tax-free income threshold and benefits taxpayers with lower or moderate income levels.

The new tax regime is suitable for individuals who do not have significant tax-saving investments or deductions. It is also beneficial for those who prefer a simple tax structure without the need to track multiple expenses and exemptions throughout the year.

What Is the Old Tax Regime

The old tax regime is the traditional system of income tax calculation that has been followed for many years. It allows taxpayers to reduce their taxable income by claiming a wide range of deductions and exemptions. While the tax rates under this system are relatively higher, the availability of these benefits can significantly lower the overall tax liability.

Under this regime, taxpayers can claim deductions for investments, insurance premiums, retirement contributions, and certain types of expenses. Exemptions related to salary components, such as house rent allowance and leave travel benefits, are also available. These provisions make the system more flexible for individuals who actively plan their finances to reduce tax outflow.

The old tax regime follows a standard slab-based structure, with tax rates increasing as income rises. It also provides different basic exemption limits for certain categories, such as senior citizens, offering additional relief to specific groups of taxpayers.

This regime is particularly useful for individuals who have significant deductions or who invest regularly in tax-saving instruments. By making use of these provisions, taxpayers can reduce their taxable income and potentially pay less tax compared to the new regime.

However, the old tax regime requires proper documentation and careful planning throughout the year. Taxpayers need to track eligible expenses and ensure that all deductions are correctly claimed at the time of filing their income tax return.

Income Tax Slabs Under the New Tax Regime

The new tax regime is the default system for individual taxpayers. It follows a simplified structure with lower tax rates but allows only limited deductions and exemptions. The objective is to make tax calculation straightforward and reduce dependency on tax-saving investments.

Under this regime, income is taxed at progressive slab rates. A higher rebate is available for lower income levels, which reduces the overall tax liability for many taxpayers.

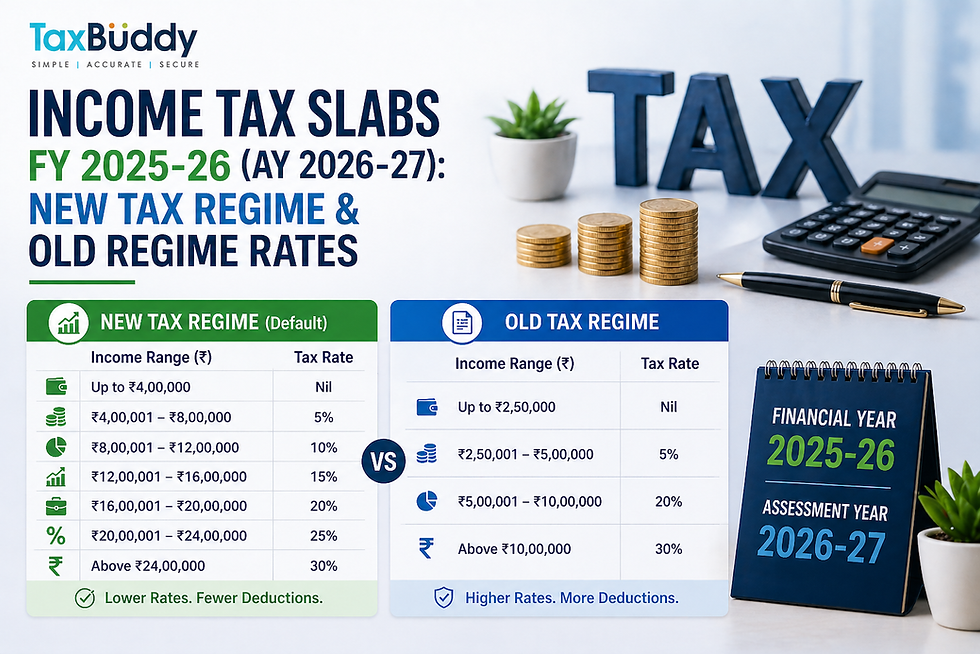

New Tax Regime Slab Rates (FY 2025-26)

Income Range | Tax Rate |

Up to ₹4,00,000 | Nil |

₹4,00,001 – ₹8,00,000 | 5% |

₹8,00,001 – ₹12,00,000 | 10% |

₹12,00,001 – ₹16,00,000 | 15% |

₹16,00,001 – ₹20,00,000 | 20% |

₹20,00,001 – ₹24,00,000 | 25% |

Above ₹24,00,000 | 30% |

Key Features of the New Tax Regime

The new tax regime applies uniformly to all individual taxpayers, regardless of age.

It offers lower tax rates across income brackets compared to the old system.

Most deductions and exemptions, such as investment-based deductions and allowances, are not available.

A standard deduction is allowed for salaried individuals, reducing taxable income.

A rebate benefit ensures that individuals with income up to a specified limit have zero tax liability.

The structure is designed to reduce complexity and simplify return filing.

The new regime is generally suitable for individuals who do not claim significant deductions or prefer a straightforward tax calculation without extensive planning.

Income Tax Slabs Under the Old Tax Regime

The old tax regime follows the traditional structure of taxation. It allows taxpayers to reduce their taxable income through various deductions and exemptions, but the tax rates are higher compared to the new regime.

This regime is often preferred by individuals who actively invest in tax-saving instruments or incur eligible expenses such as insurance premiums, home loan interest, or rent.

Old Tax Regime Slab Rates (FY 2025-26)

For Individuals Below 60 Years and NRIs

Income Range | Tax Rate |

Up to ₹2,50,000 | Nil |

₹2,50,001 – ₹5,00,000 | 5% |

₹5,00,001 – ₹10,00,000 | 20% |

Above ₹10,00,000 | 30% |

For Senior Citizens (60–80 Years)

Income Range | Tax Rate |

Up to ₹3,00,000 | Nil |

₹3,00,001 – ₹5,00,000 | 5% |

₹5,00,001 – ₹10,00,000 | 20% |

Above ₹10,00,000 | 30% |

For Super Senior Citizens (Above 80 Years)

Income Range | Tax Rate |

Up to ₹5,00,000 | Nil |

₹5,00,001 – ₹10,00,000 | 20% |

Above ₹10,00,000 | 30% |

Key Features of the Old Tax Regime

The regime offers multiple deductions and exemptions that reduce taxable income.

Common deductions include investments, insurance premiums, and specific expenses.

Salary-related benefits such as house rent allowance and leave travel allowance can be claimed.

Taxpayers can use structured tax planning to lower their overall liability.

The slab rates are higher, but the effective tax can be reduced through eligible deductions.

The old regime is generally more beneficial for individuals who have significant investments or expenses that qualify for tax deductions and want to optimise their tax liability through planning.

Key Differences Between New and Old Tax Regime

The new and old tax regimes differ in terms of tax rates, availability of deductions, and overall approach to tax calculation. While the new regime focuses on simplicity and lower tax rates, the old regime allows taxpayers to reduce their taxable income through various deductions and exemptions.

The following table highlights the key differences between the two regimes:

Particulars | New Tax Regime | Old Tax Regime |

Tax Rates | Lower slab rates | Higher slab rates |

Deductions | Very limited deductions | Wide range of deductions available |

Standard Deduction | Available | Available |

Exemptions (HRA, LTA, etc.) | Mostly not allowed | Allowed |

Default Option | Yes | No |

Complexity | Simple and easy to calculate | Requires tax planning |

Suitable For | Individuals with fewer deductions | Individuals with investments and eligible deductions |

The new tax regime is designed to reduce the effort involved in tax calculation. Since most deductions are not available, the taxable income is calculated directly from gross income with minimal adjustments. This reduces the chances of errors and simplifies the filing process.

In contrast, the old tax regime allows taxpayers to lower their taxable income by claiming deductions such as investments, insurance premiums, and housing-related expenses. While this can result in lower tax liability, it requires proper documentation and planning throughout the financial year.

Another important difference is the default selection. The new tax regime is automatically applied unless the taxpayer actively chooses the old regime. This makes it necessary to evaluate both options before filing the return.

Deductions and Exemptions Under Both Regimes

Deductions and exemptions play a significant role in determining the final tax liability under each regime. The availability of these benefits is one of the main factors that differentiate the two systems.

Under the old tax regime, taxpayers can claim multiple deductions and exemptions to reduce their taxable income. These benefits are linked to specific expenses, investments, or income categories.

Some of the commonly available deductions and exemptions under the old regime include:

Investments in specified instruments, such as a provident fund and life insurance

Health insurance premiums

Interest on education loans

Donations to eligible institutions

House rent allowance (HRA)

Leave travel allowance (LTA)

Interest on housing loans

These deductions encourage savings and long-term financial planning, but they also require proper tracking and documentation.

Under the new tax regime, most of these deductions and exemptions are not available. The idea is to offer lower tax rates in exchange for removing multiple conditions and compliance requirements.

However, certain benefits are still allowed under the new regime, such as:

Standard deduction for salaried individuals

Employer contribution to retirement schemes within prescribed limits

Specific exemptions notified under tax rules

The following table provides a simple comparison:

Type of Benefit | New Tax Regime | Old Tax Regime |

Investment-based deductions | Not allowed | Allowed |

Salary exemptions (HRA, LTA) | Not allowed | Allowed |

Standard deduction | Allowed | Allowed |

Insurance and loan deductions | Limited | Allowed |

Tax-saving opportunities | Minimal | Significant |

The choice between the two regimes depends largely on whether a taxpayer is able to claim sufficient deductions. If the total deductions are high, the old regime may result in lower tax liability. If deductions are minimal, the new regime may be more beneficial due to lower tax rates and simplified computation.

Tax Rebate and Zero Tax Limit

The tax rebate is a relief provided to reduce the final tax payable for individuals with lower incomes. Under the income tax law, this benefit ensures that taxpayers within a specified income limit do not have to pay any tax after applying the rebate.

For the financial year 2025–26, the rebate provisions under the new tax regime have been structured in a way that significantly increases the tax-free income threshold. Even though tax slabs apply from lower income levels, the rebate ensures that individuals within a certain income range end up with zero tax liability.

Under the new tax regime, the rebate is available to resident individuals whose total income falls within the specified limit. After calculating tax based on slab rates, the rebate reduces the tax liability to zero, subject to the maximum rebate allowed. This effectively increases the practical tax-free limit beyond the basic exemption level.

In comparison, the old tax regime also provides a rebate, but the threshold is lower. Taxpayers under this regime can claim the rebate only if their income remains within the specified limit after claiming deductions. As a result, the overall tax-free income level under the old regime is comparatively lower.

The key difference lies in how the rebate interacts with deductions. Under the old regime, taxpayers relied on deductions to reduce taxable income and qualify for the rebate. Under the new regime, fewer deductions are available, but the higher rebate threshold compensates by offering a wider zero-tax range.

The following table highlights the difference in rebate impact under both regimes:

Particulars | New Tax Regime | Old Tax Regime |

Rebate availability | Available for resident individuals | Available for resident individuals |

Dependence on deductions | Limited deductions | Wide range of deductions |

Effective zero-tax income | Higher due to rebate structure | Lower unless deductions are maximized |

Complexity | Lower | Higher due to planning requirements |

The concept of a zero tax limit is therefore not only linked to the basic exemption limit but also depends on the rebate available. Taxpayers should consider both factors together while estimating their final tax liability.

Which Tax Regime Is Better for You

Choosing between the new and old tax regimes depends on the structure of your income, the level of deductions you claim, and your overall financial planning approach. Both regimes are designed to suit different types of taxpayers, and the better option varies from person to person.

The new tax regime is generally more suitable for individuals who prefer a simplified tax structure. It offers lower tax rates and reduces the need to track multiple deductions and exemptions. Taxpayers with minimal investments or those who do not actively claim deductions may find this regime more beneficial.

On the other hand, the old tax regime is better suited for individuals who make use of various deductions and exemptions. If you have significant investments, insurance premiums, housing loan interest, or other eligible expenses, the old regime can help reduce your taxable income and overall tax liability.

The choice also depends on income level. For middle-income taxpayers who claim standard deductions but do not have many additional exemptions, the new regime may provide a better outcome. However, for taxpayers with higher deductions, the old regime may still result in lower tax liability despite higher slab rates.

The following table provides a practical comparison:

Scenario | Better Regime |

Limited deductions and simple income structure | New Tax Regime |

High deductions through investments and expenses | Old Tax Regime |

Preference for ease of filing | New Tax Regime |

Active tax planning and investment strategy | Old Tax Regime |

It is important to calculate tax liability under both regimes before making a decision. A simple comparison using your income and eligible deductions can help identify the option that results in lower tax.

The decision is not only about tax savings but also about financial behaviour. The new regime reduces dependency on tax-saving investments, while the old regime encourages structured savings and long-term financial planning.

How to Choose Between New and Old Tax Regime

Choosing between the new and old tax regimes depends on how your income is structured and whether you actively claim deductions. Both options remain available for FY 2025–26, and the right choice varies from one taxpayer to another.

The new tax regime offers lower tax rates and a simpler structure, but removes most deductions. The old tax regime allows a wide range of deductions and exemptions, but applies higher tax rates. The decision should be based on a clear comparison of total tax liability under both systems.

A practical approach is to evaluate the following factors:

1. Total Income Level Your overall income plays a key role in deciding the better option. Under the new regime, lower tax rates and rebate benefits can reduce tax liability for individuals with moderate income levels. However, at higher income levels, deductions available under the old regime can provide significant tax savings.

2. Deductions and Exemptions Claimed If you regularly claim deductions such as investments, insurance premiums, home loan interest, or salary-related exemptions, the old regime may result in lower tax liability. On the other hand, if you do not have substantial deductions, the new regime may be more beneficial.

3. Investment Pattern The old regime encourages tax-saving investments, while the new regime does not depend on them. Taxpayers who prefer disciplined savings through eligible deductions may benefit from the old regime. Those who prefer flexibility in spending and investing may find the new regime more suitable.

4. Simplicity and Compliance The new regime simplifies tax calculation and reduces documentation requirements. It is easier to follow, especially for individuals who do not want to track multiple deductions. The old regime requires proper documentation and planning to claim benefits.

5. Tax Calculation Comparison Before making a decision, it is important to calculate tax liability under both regimes using actual income and deductions. This comparison provides a clear view of which option results in lower tax payable.

When the New Regime May Be Suitable

Limited or no deductions claimed

Preference for simpler tax filing

Lower or moderate income levels

When the Old Regime May Be Suitable

Significant deductions and exemptions claimed

Higher investments in eligible instruments

Need to reduce taxable income through planning

Taxpayers should review their situation every year, as changes in income, expenses, or investment patterns can impact the final decision.

Conclusion

The income tax structure for FY 2025–26 continues to provide two options for taxpayers. The new tax regime focuses on lower tax rates and simplicity, while the old tax regime allows deductions and exemptions to reduce taxable income.

The choice between the two regimes is not fixed and should be based on actual financial data. Taxpayers who prioritise ease of filing and do not rely on deductions may prefer the new regime. Those who actively use deductions and exemptions to manage their tax liability may find the old regime more beneficial.

A proper comparison of tax payable under both regimes is essential before filing the return. This ensures that the selected option aligns with the taxpayer’s income structure and financial planning approach.

FAQs

Q1. What are the income tax slabs for FY 2025-26?

Income tax slabs for FY 2025–26 differ under the new and old tax regimes. The new regime follows a revised slab structure with lower tax rates and a higher rebate limit, while the old regime continues with traditional slab rates and age-based exemptions. Taxpayers can choose either regime based on what results in lower tax liability.

Q2. Which tax regime is the default option?

The new tax regime is the default option. This means that if a taxpayer does not specifically choose a regime while filing their return, the new tax regime will automatically apply. However, taxpayers can opt for the old regime if it is more beneficial.

Q3. Can I switch between tax regimes every year?

Salaried individuals can switch between the new and old tax regimes every year at the time of filing their return. However, individuals with business or professional income are allowed limited switches. Once they opt out of the new regime, they may not be able to switch back frequently.

Q4. What deductions are allowed under the old tax regime?

The old tax regime allows a wide range of deductions and exemptions. These include deductions for investments, insurance premiums, home loan interest, education loan interest, and various salary-related exemptions. These deductions help reduce taxable income and lower the overall tax liability.

Q5. What deductions are allowed under the new tax regime?

The new tax regime allows only a limited number of deductions. Most common deductions are not available. However, certain benefits such as the standard deduction for salaried individuals and specific employer contributions may still be allowed.

Q6. What is the zero tax limit under the new tax regime?

Under the new tax regime, individuals can have zero tax liability up to a specified income level due to the availability of a rebate. This effectively increases the tax-free income threshold, making the new regime more beneficial for individuals with lower or moderate income levels.

Q7. Is the standard deduction available in both tax regimes?

Yes, the standard deduction is available under both the new and old tax regimes for salaried individuals. This deduction reduces taxable salary income without requiring any specific investment or expense.

Q8. Which tax regime is better for salaried individuals?

The better regime depends on the level of deductions claimed. Salaried individuals who claim significant deductions such as HRA, investments, and loan-related benefits may find the old regime more beneficial. Those with fewer deductions may benefit from the new regime due to lower tax rates.

Q9. Which tax regime is better for high-income taxpayers?

For high-income taxpayers, the choice depends on the amount of deductions claimed. If deductions are substantial, the old regime may reduce taxable income significantly. If deductions are minimal, the new regime may result in a lower tax liability due to its structured rates.

Q10. Can I choose a different tax regime while filing my return?

Yes, taxpayers can choose their preferred tax regime while filing their income tax return. The selection is made during the filing process, and it determines how income is taxed for that financial year.

Q11. Can I change my tax regime after filing my return?

Once the income tax return is filed, the choice of tax regime generally cannot be changed. However, if a revised return is filed within the allowed time, changes may be possible depending on the applicable rules.

Q12. Does the new tax regime eliminate all exemptions?

The new tax regime removes most exemptions and deductions, but not all. Certain benefits, such as the standard deduction and specific allowances, may still be available. The focus is on simplifying tax calculations rather than eliminating all benefits.

Q13. Is it mandatory to invest under the old tax regime?

No, it is not mandatory to invest under the old tax regime. However, investments and expenses that qualify for deductions can help reduce taxable income. Taxpayers who do not make such investments may not fully benefit from the old regime.

Q14. How should I compare both tax regimes before choosing?

Taxpayers should calculate their total tax liability under both regimes using their actual income and deductions. This comparison helps identify which regime results in lower tax payable. Using tax calculators or professional assistance can improve accuracy.

Q15. Does choosing a tax regime affect future tax planning?

Yes, the choice of tax regime can influence financial planning decisions. The old regime encourages investment in tax-saving instruments, while the new regime provides flexibility in spending and investment choices. Taxpayers should consider their long-term financial goals while selecting a regime.

Comments