Common Section 10 Exemptions for Salaried Employees

- Dipali Waghmode

- Nov 10, 2025

- 8 min read

Section 10 of the Income Tax Act, 1961, offers valuable exemptions that reduce taxable income for salaried employees. These provisions include allowances, reimbursements, and retirement benefits that ease the financial burden while improving compliance efficiency. Understanding these exemptions is essential during salary structuring, bank account verification, and year-end tax planning. By optimizing these benefits under the correct regime, employees can achieve better in-hand income and financial clarity.

Table of Contents

Overview of Section 10 Exemptions

Section 10 of the Income Tax Act, 1961, defines specific types of income that are not included in the total taxable income of an employee. These exemptions are designed to reduce the financial burden on salaried individuals by exempting certain allowances, reimbursements, and benefits from taxation. For instance, allowances such as House Rent Allowance (HRA), Leave Travel Allowance (LTA), and educational allowances are excluded from the taxable salary if the prescribed conditions are met. This section plays a crucial role in salary structuring and tax planning, ensuring that employees can retain a higher portion of their earnings while remaining fully compliant with tax laws.

Key Section 10 Exemptions for Salaried Employees

Section 10 offers several exemptions that directly benefit salaried employees. The most commonly claimed ones include:

House Rent Allowance (HRA) [Section 10(13A)]: Employees receiving HRA can claim exemption based on actual rent paid, city of residence, and salary structure. The exemption is limited to the least of actual HRA received, rent paid minus 10% of salary, or 50% of salary for metro cities (40% for non-metro).

Leave Travel Allowance (LTA) [Section 10(5)]: Employees can claim exemption on travel expenses within India for themselves and their family. This is limited to two trips in a block of four years and requires submission of travel proofs.

Gratuity, Pension, and Leave Encashment [Sections 10(10), 10(10A), 10(10AA)]: These retirement benefits are either fully or partially exempt depending on employment type (government or non-government) and prescribed limits.

Special Allowances and Perquisites [Section 10(14)]: Includes allowances for travel, research, or uniforms. The exemption is limited to the amount actually spent for official purposes.

Provident Fund and Life Insurance Proceeds [Sections 10(11) and 10(10D)]: Interest earned on recognized provident funds and maturity proceeds from life insurance policies are exempt subject to specific conditions on premium limits and contribution periods.

Agricultural Income and Miscellaneous Exemptions: Income from agricultural activities is fully exempt but must be disclosed for rate computation. Certain allowances, such as children’s education or hostel allowance, are also partially exempt up to specified monthly limits.

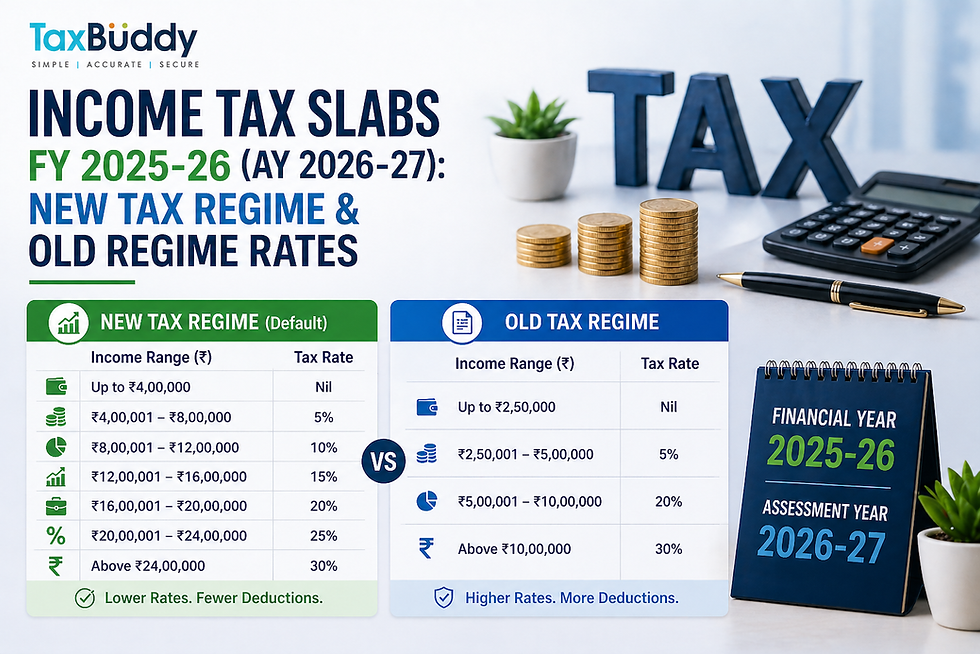

Is Section 10 Allowed in the New Tax Regime?

Under the new tax regime introduced in Section 115BAC, most of the traditional exemptions under Section 10 are no longer available. The new regime offers lower slab rates but removes popular benefits such as HRA, LTA, and professional tax deduction. However, a few exemptions like the employer’s contribution to the National Pension Scheme (NPS), gratuity, and leave encashment remain available.

In contrast, the old regime allows employees to claim a wide range of Section 10 exemptions, making it more beneficial for those with significant allowances or deductions. Employees should calculate their net tax liability under both regimes before making a choice each financial year.

Documentation Required to Claim Section 10 Exemptions

To claim exemptions under Section 10, salaried employees must maintain valid proof and submit them to their employers during tax declaration. Common documentation includes:

Rent receipts, rental agreements, and landlord’s PAN for HRA claims

Travel tickets and bills for LTA claims

School or college fee receipts for children’s education allowance

Employer settlement letters for gratuity and pension benefits

Provident Fund statements for exemption validation

Employers verify these documents before computing TDS on salary, ensuring that only eligible exemptions are claimed.

Common Mistakes While Claiming Section 10 Exemptions

Many employees lose out on exemptions due to small errors. The most frequent mistakes include:

Submitting incomplete documentation or claiming exemptions without valid proof

Not disclosing exempt income in the ITR, leading to processing delays or tax notices

Claiming exemptions under the old regime while opting for the new one

Missing deadlines for declaration or proof submission during payroll processing

Reviewing documents and verifying eligibility under the chosen regime helps avoid these issues and ensures compliance with tax rules.

Importance of Disclosing Exempt Income in ITR

Even if certain incomes are exempt under Section 10, they must still be disclosed in the Income Tax Return. This disclosure ensures transparency and helps the Income Tax Department verify income sources. Non-disclosure of exempt income can trigger discrepancies in AIS (Annual Information Statement) or tax notices during assessment. Reporting such income correctly also contributes to smoother refund processing and reduced chances of audit queries.

How TaxBuddy Simplifies Section 10 Exemption Claims

TaxBuddy simplifies the entire process of claiming Section 10 exemptions by integrating automation and expert guidance into its platform. Salaried individuals can upload salary slips, Form 16, and proof documents directly to the TaxBuddy dashboard, where the system automatically identifies eligible exemptions based on the latest rules. The platform’s AI-driven engine performs real-time validation and ensures accurate tax computation under both regimes. For those with complex cases—such as multiple allowances or variable salary components—TaxBuddy’s expert-assisted filing ensures every eligible benefit is claimed correctly, minimizing the chances of tax errors or notices.

Conclusion

Section 10 exemptions remain one of the most effective tools for salaried employees to reduce taxable income and maximize savings. Proper documentation, awareness of eligibility, and understanding regime-specific applicability are crucial to claiming these benefits. With the help of intelligent platforms like TaxBuddy, managing exemptions and filing taxes has become more efficient and accurate.

For anyone looking for assistance in tax filing, it is highly recommended to download the TaxBuddy mobile app for a simplified, secure, and hassle-free experience.

FAQs

Q1. Does TaxBuddy offer both self-filing and expert-assisted plans for ITR filing, or only expert-assisted options?

TaxBuddy provides flexibility for all types of taxpayers by offering both self-filing and expert-assisted plans. The self-filing option allows users to upload Form 16 and other documents for automatic data extraction and AI-based validation, ensuring error-free returns. For individuals with complex tax matters—such as multiple exemptions under Section 10, capital gains, or NRI income—the expert-assisted plan offers personalized review and end-to-end filing by qualified professionals, ensuring every eligible exemption and deduction is correctly claimed.

Q2. Which is the best site to file ITR?

While the official Income Tax Department portal remains the primary government platform, many taxpayers prefer using AI-enabled platforms like TaxBuddy for a more seamless filing experience. TaxBuddy’s platform simplifies the process through automated validation, real-time error detection, and expert-backed review, ensuring faster and more accurate returns. It also helps optimize tax benefits under Section 10 and other provisions, making it one of the most reliable online filing platforms in India.

Q3. Where to file an income tax return?

Taxpayers can file their ITR through two main options: the official e-filing portal of the Income Tax Department or trusted private platforms like TaxBuddy. The government portal is suitable for experienced users who prefer manual filing, while TaxBuddy is ideal for individuals seeking an intuitive, guided process. Through its AI-driven engine and expert review system, TaxBuddy ensures compliance, error-free computation, and maximum utilization of Section 10 exemptions and other tax-saving provisions.

Q4. Which Section 10 exemptions are most relevant for payroll or account setup?

The most relevant Section 10 exemptions for payroll and account setup include House Rent Allowance (HRA), Leave Travel Allowance (LTA), children’s education allowance, and special allowances such as uniform or conveyance allowance. These exemptions directly impact the employee’s take-home salary and help optimize net taxable income. Employers usually require declarations and proofs for these exemptions at the beginning of each financial year during salary structuring or when opening new payroll accounts.

Q5. Are HRA and LTA exemptions available under the new regime?

No, HRA and LTA exemptions are not available under the new tax regime as per Section 115BAC. The new regime offers lower tax rates but excludes most traditional exemptions and deductions under Section 10. However, employees can still claim these exemptions if they choose the old regime. It is advisable to compare both regimes based on income structure, available allowances, and deductions before selecting one. TaxBuddy’s calculator can help estimate which regime offers better tax savings.

Q6. What documents are required to claim Section 10 exemptions?

To claim Section 10 exemptions, employees must submit valid supporting documents to their employer. These include rent receipts or rental agreements for HRA, travel tickets and invoices for LTA, and fee receipts for children’s education allowance. Pension, gratuity, and provident fund claims require settlement letters or PF statements. Submitting these documents accurately ensures that eligible exemptions are considered during TDS computation and reflected in Form 16, avoiding discrepancies while filing ITR.

Q7. Can multiple Section 10 exemptions be claimed simultaneously?

Yes, multiple Section 10 exemptions can be claimed together under the old tax regime, provided all conditions are satisfied and proofs are submitted. For example, an employee can simultaneously claim HRA, LTA, and children’s education allowance. However, overlapping claims or duplicate submissions should be avoided. Each exemption has its own eligibility criteria, and the claimed amounts must align with the actual expenses incurred. Platforms like TaxBuddy ensure that no ineligible or duplicate claims are made during filing.

Q8. Is agricultural income under Section 10 relevant for salaried employees?

Agricultural income under Section 10(1) is fully exempt from tax. For salaried employees, it becomes relevant only if they earn additional income from agricultural activities. While it is not taxable, it must be reported in the ITR for rate computation if the total income exceeds ₹2.5 lakh. Proper disclosure ensures that tax rates are calculated correctly and avoids mismatches in income reporting.

Q9. Why must exempt income be disclosed in ITR?

Even though exempt incomes are not taxable, they must still be disclosed in the Income Tax Return under the “Exempt Income” section. This disclosure helps maintain transparency and ensures the Income Tax Department can reconcile income records. Non-disclosure may lead to discrepancies in AIS or TIS (Taxpayer Information Summary), triggering verification notices or delays in refund processing. Platforms like TaxBuddy automatically categorize and disclose such incomes correctly during e-filing.

Q10. How does one compare Section 10 exemptions under old vs. new regime?

The old tax regime allows a wide range of exemptions such as HRA, LTA, standard deduction, and professional tax relief, making it suitable for individuals with multiple allowances. The new tax regime offers lower tax rates but removes most exemptions to simplify filing. The best approach is to calculate total taxable income under both regimes and select the one with the lower tax liability. TaxBuddy provides side-by-side comparisons and personalized suggestions based on salary structure and exemptions.

Q11. Can life insurance proceeds be claimed as exempt under Section 10(10D)?

Yes, maturity proceeds from life insurance policies are exempt under Section 10(10D) if the annual premium does not exceed 10% of the sum assured (for policies issued after April 1, 2012). However, if the premium crosses this threshold, the maturity amount becomes taxable. Death benefits are always exempt regardless of the premium amount. TaxBuddy’s system automatically identifies whether a policy qualifies for exemption while preparing the ITR.

Q12. How does TaxBuddy help in tracking and filing Section 10 exemptions?

TaxBuddy helps users manage Section 10 exemptions efficiently through its AI-powered filing interface. It automatically extracts exemption details from Form 16, salary slips, and uploaded documents. The platform ensures each exemption—like HRA, LTA, and gratuity—is validated against current tax rules. For complex cases, TaxBuddy’s expert-assisted service provides one-on-one consultation, helping users avoid mistakes and maximize tax benefits. This ensures smooth, compliant, and error-free income tax filing every financial year.

Comments