How TaxBuddy DIY Filing Maintains Continuity Across Past and Current Returns

- CA Pratik Bharda

- Mar 10

- 8 min read

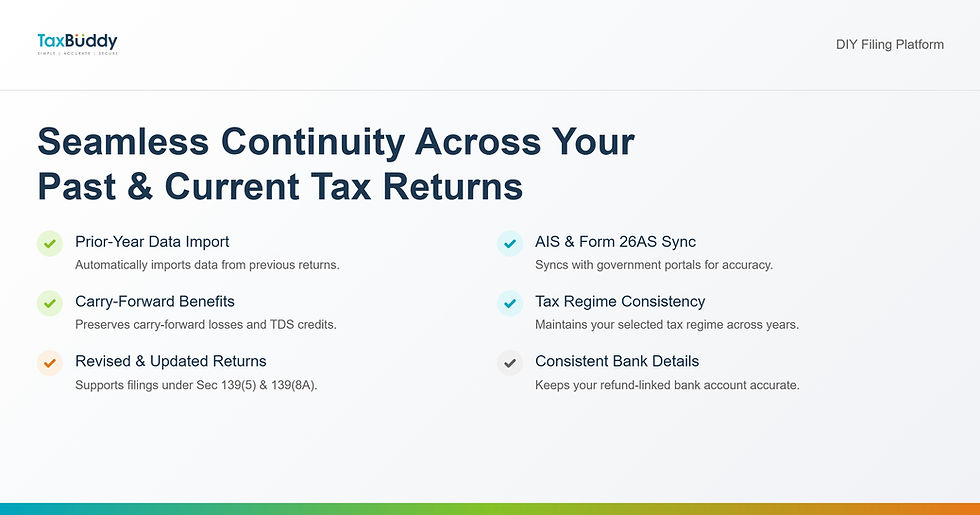

TaxBuddy DIY Filing maintains continuity between past and current Income Tax Returns by importing prior-year data, syncing with AIS and Form 26AS, and preserving carry-forward losses, TDS credits, and regime selections. It reduces reporting errors, supports revised and updated returns under Sections 139(5) and 139(8A), and ensures refund-linked bank details remain accurate across years. By aligning historical return data with current-year disclosures, the platform enables structured and compliant tax filing without disrupting previously reported information or statutory carry-forward benefits under the Income Tax Act, 1961.

TaxBuddy DIY Filing maintains continuity across past and current returns by automatically importing prior-year return data, syncing it with AIS and CPC records, tracking carry-forward losses and TDS credits, preserving tax regime selections, and ensuring bank and refund details remain consistent, thereby reducing errors and maintaining compliance under Sections 139(5), 139(8A), and related provisions of the Income Tax Act, 1961.

Table of Contents

How TaxBuddy DIY Filing Ensures Continuity Across Financial Years

Continuity in income tax filing means that information declared in earlier returns flows correctly into the current assessment year without duplication, omission, or mismatch. TaxBuddy DIY Filing maintains this continuity by syncing prior ITR data, AIS records, TDS credits, bank details, and carry-forward losses into the present-year workflow. Instead of treating each assessment year as an isolated filing, the system connects historical disclosures with current obligations under the Income Tax Act, 1961. This reduces the risk of refund delays, lapses, or notices arising from inconsistent reporting across years.

Auto-Population of Data from Previous ITRs and AIS

TaxBuddy integrates data from the Income Tax Department’s portal and the Annual Information Statement. Salary details, capital gains, deductions, interest income, and TDS credits are auto-populated based on prior filings and AIS updates.

This auto-import process serves two purposes:

It reduces manual data entry errors.

It ensures consistency in recurring disclosures such as house property details, depreciation schedules, and carry-forward balances.

Users are still prompted to verify the information before submission, ensuring accuracy without disrupting continuity.

How TaxBuddy DIY Filing Maintains Carry-Forward of Losses

Loss carry-forward is one of the most critical continuity elements in tax filing. Business losses under Section 72, capital losses, and house property losses must be correctly reported year after year to remain valid.

TaxBuddy pulls forward previously declared losses and maps them against current-year set-off rules. The system tracks:

Remaining loss balance

Set-off eligibility in the current year

Expiry timelines under statutory limits

This structured tracking prevents accidental forfeiture of eligible losses.

Handling TDS Credits and CPC Updates Without Mismatch

TDS continuity depends on synchronisation with Form 26AS and AIS. TaxBuddy aligns credits with CPC updates, especially those reflected after quarterly filings or post-May 31 reconciliations.

If a mismatch appears between prior-year carry-forward credits and current-year records, the system flags it before submission. This reduces the chances of short credit issues and post-filing rectifications.

Revised Returns Under Section 139(5) and Data Supersession

When a revised return is filed under Section 139(5), the new filing replaces the original return. TaxBuddy imports the original ITR, highlights editable fields, and ensures that the revised submission supersedes the previous one properly.

This approach maintains version control across assessment years and avoids duplication of income or deduction entries.

Updated Returns Under Section 139(8A) and Multi-Year Continuity

Section 139(8A) allows updated returns within the prescribed time limit. TaxBuddy supports multi-year filing, allowing users to update prior years without disrupting current-year continuity.

Historical data is preserved, and updated disclosures are reflected systematically. This ensures compliance while maintaining alignment with previous filings.

Belated Returns and Historical Data Alignment

Belated returns must still preserve carry-forward eligibility where permitted. TaxBuddy ensures that even when a return is filed after the due date, eligible components such as TDS credits and regime selections remain aligned with statutory provisions.

The system also flags limitations where carry-forward benefits may not apply due to delayed filing.

Maintaining Tax Regime Continuity in TaxBuddy DIY Filing

Tax regime selection has long-term implications. TaxBuddy references prior-year regime choices and prompts users to confirm or change the regime as permitted under law.

This prevents inconsistent selection across years and helps maintain continuity in deduction planning, especially when switching between regimes requires specific compliance conditions.

Bank Account Continuity and Refund Tracking Under Section 244A

Refund processing under Section 244A requires accurate bank linkage. TaxBuddy pre-fills bank account details from earlier returns or AIS records and verifies PAN-linked status.

If any account mismatch is detected, the system prompts correction before submission. This ensures that refund continuity remains intact and interest eligibility is not affected.

How TaxBuddy Handles PAN-Linked Bank Changes from Past ITRs

When bank details differ from prior filings, TaxBuddy cross-checks current AIS and portal data. If a new account is introduced, users are prompted to upload proof such as a passbook or cancelled cheque.

This structured verification avoids refund rejection due to outdated or inactive accounts.

Importing Original ITR for Revision Without Data Disruption

Revision workflows require careful handling to avoid overwriting historical disclosures incorrectly. TaxBuddy imports the original ITR file and allows selective modification.

Changes are tracked, ensuring that only intended corrections are made without disturbing unrelated fields.

Ensuring Compliance with Schedule FA and High-Value Transaction Reporting

Continuity is especially important for foreign assets reported in Schedule FA and high-value transactions reflected in AIS. TaxBuddy carries forward asset disclosures where applicable and prompts updates only when changes occur.

This ensures year-on-year consistency in global asset reporting obligations.

Common Continuity Issues in Income Tax Filing and How TaxBuddy Resolves Them

Frequent continuity errors include:

Incorrect carry-forward loss balances

Duplicate TDS reporting

Regime inconsistency

Bank account mismatches

Missing revised return references

TaxBuddy addresses these issues through structured validation prompts and historical data mapping.

Data Verification Prompts and Error Flags Across Assessment Years

The system uses cross-year validation checks. If income figures differ substantially from prior returns, or if deduction patterns change unexpectedly, prompts appear for confirmation.

This review mechanism helps maintain logical consistency across financial years.

Role of AIS and Form 26AS in Maintaining Filing Consistency

AIS and Form 26AS serve as centralised financial records. TaxBuddy aligns imported data with these records to ensure reporting consistency.

If new transactions appear in AIS that were not part of earlier returns, users are guided to disclose or reconcile them before submission.

Continuity in Penalty and Late Fee Tracking Under Section 234F

Late filing fees under Section 234F and related interest provisions are automatically computed where applicable.

If prior-year delays exist, the system reflects them accurately without affecting current-year compliance calculations.

Multi-Year Filing Support and Historical Record Preservation

TaxBuddy supports filing across multiple assessment years within one ecosystem. Historical returns remain accessible for review, revision, or update.

This centralised structure ensures that loss schedules, regime choices, and disclosures remain connected across years.

Security, Validation, and System-Based Checks in DIY Filing

Continuity requires both data accuracy and security. TaxBuddy incorporates encrypted data transfer, validation logic, and structured review steps before final submission.

Each year’s return builds upon prior data while maintaining statutory compliance safeguards.

Conclusion

Continuity across financial years is essential for accurate carry-forward, refund processing, and compliance with the Income Tax Act. TaxBuddy DIY Filing connects historical returns, AIS data, and statutory provisions into one structured workflow, reducing errors and preserving year-on-year alignment. For taxpayers seeking consistent and error-free filing across multiple assessment years, it is advisable to download the TaxBuddy mobile app for a simplified, secure, and hassle-free experience:

FAQs

Q1. How does TaxBuddy DIY Filing import data from previous Income Tax Returns?

TaxBuddy connects with the Income Tax Department’s portal and retrieves prior-year return data such as income heads, deductions, carry-forward losses, tax regime selection, and bank details. It also syncs with AIS and Form 26AS to cross-verify information. This ensures that recurring disclosures, such as house property details or depreciation schedules, remain consistent without requiring manual re-entry every year.

Q2. Can TaxBuddy maintain continuity of carry-forward losses across multiple years?

Yes. The system tracks business losses, capital losses, and house property losses declared in earlier returns. It automatically reflects the remaining eligible balance in the current year and checks set-off eligibility under the Income Tax Act. This prevents accidental loss of carry-forward benefits due to reporting errors.

Q3. How does TaxBuddy handle TDS credit mismatches from past returns?

TaxBuddy aligns TDS credits with AIS and Form 26AS records. If credits reflected in prior returns differ from updated CPC records, the system flags the mismatch before submission. This helps avoid short credit claims and post-filing rectification requests.

Q4. Does TaxBuddy support revised returns under Section 139(5) without disturbing historical data?

Yes. When filing a revised return, the original ITR is imported and marked as the base version. Users can modify only the necessary fields, and the revised return automatically supersedes the earlier one. This preserves the filing history while maintaining legal compliance.

Q5. Can updated returns under Section 139(8A) be filed while maintaining continuity with current filings?

TaxBuddy supports updated returns within the permitted time frame. Historical disclosures are preserved, and any additional income or corrections made in updated returns are aligned with current-year data to prevent inconsistencies across assessment years.

Q6. How does the platform ensure tax regime continuity across financial years?

The system references the previous year’s tax regime selection and prompts confirmation or change as allowed under law. This reduces the risk of inconsistent regime choices and ensures that deductions or exemptions are applied correctly based on the selected regime.

Q7. What happens if bank account details have changed from earlier ITRs?

TaxBuddy cross-checks PAN-linked bank accounts with AIS and portal records. If changes are detected, it prompts re-verification and document upload. This ensures refund continuity under Section 244A and avoids rejections due to outdated account details.

Q8. Does TaxBuddy track late filing fees and penalties from previous years?

Yes. The system computes applicable late filing fees under Section 234F and relevant interest provisions. It ensures that prior-year penalties are properly reflected without affecting the accuracy of current-year tax calculations.

Q9. How does TaxBuddy maintain consistency in reporting foreign assets and high-value transactions?

For disclosures such as Schedule FA and high-value transactions appearing in AIS, the platform carries forward relevant information and prompts updates only when required. This ensures year-on-year compliance in reporting global income and asset details.

Q10. Can belated returns still preserve continuity in carry-forward and disclosures?

Where legally permitted, TaxBuddy aligns belated return data with prior disclosures. It flags any limitations related to carry-forward eligibility and ensures that TDS credits and regime choices remain accurately reflected.

Q11. How are data discrepancies across assessment years identified?

The platform uses validation checks that compare income trends, deduction patterns, and loss balances across years. If significant deviations are detected, prompts appear for confirmation. This structured review process reduces the risk of notices due to inconsistent reporting.

Q12. Is multi-year tax filing supported within the same system?

Yes. TaxBuddy allows users to access, review, revise, or update multiple assessment years within one ecosystem. Historical records, carry-forward balances, and filing versions are preserved, ensuring seamless continuity across financial years.

Comments