10 Common ITR Filing Mistakes to Avoid in 2025

- PRITI SIRDESHMUKH

- Nov 12, 2025

- 8 min read

Filing an Income Tax Return in 2025 demands precision. New e-filing formats, AI-based data checks, and stricter compliance rules mean that even a small oversight—wrong form selection, missed income, or unverified filing—can stall your refund or trigger scrutiny. With timely preparation and awareness, taxpayers can file accurately and avoid penalties.

Table of Contents

Choosing the Wrong ITR Form

Selecting the correct ITR form is the first and most critical step in the filing process. Each form caters to different types of income and taxpayer categories. Filing under the wrong form may result in your return being marked defective under Section 139(9), leading to delays and re-submission. For instance, salaried individuals with income below ₹50 lakh and no business income should use ITR-1, while freelancers, professionals, and business owners should opt for ITR-3 or ITR-4. Before submission, review your income sources and residential status carefully to choose the correct form.

Not Reconciling Income with AIS and Form 26AS

Your Annual Information Statement (AIS) and Form 26AS record income details, TDS, and transactions reported to the Income Tax Department. Many taxpayers skip cross-verifying these before filing, resulting in mismatches between reported income and departmental data. Such discrepancies often trigger adjustment notices or delayed refunds. Always download Form 26AS and AIS from the e-filing portal, compare them with your Form 16 and bank statements, and resolve any differences before submitting your return.

Failing to Report All Income Sources

A common mistake is omitting smaller or secondary income streams, such as interest from savings accounts, fixed deposits, dividends, rental income, or freelance earnings. Even exempt income like agricultural earnings or PPF interest should be disclosed under the relevant section. Incomplete disclosure can attract scrutiny or penalty notices under Section 270A for underreporting. Ensure that every source of income—no matter how minor—is reported accurately for transparency and compliance.

Incorrect Deduction or Exemption Claims

Taxpayers often make errors when claiming deductions under Sections 80C, 80D, or 80G—either by claiming beyond the limit or failing to maintain valid proofs. Submitting incorrect claims may result in disallowance or penalty. Always retain investment proofs such as insurance receipts, ELSS statements, or donation certificates. Claim only eligible deductions up to the prescribed limits, and verify them through reliable tax platforms like TaxBuddy, which automatically checks your eligibility and prevents overclaiming.

Entering Wrong Bank Account Details

Incorrect bank account numbers, IFSC codes, or mismatched names can delay or block refund processing. It’s essential to provide an active, pre-validated account linked to your PAN. The Income Tax Department only credits refunds to validated bank accounts. Before submission, log in to the e-filing portal, confirm your account details, and validate through net banking or Aadhaar-linked verification to avoid failed transactions.

Forgetting to E-Verify the Return

Filing your ITR without e-verification renders it invalid. The department does not process unverified returns, and refunds remain on hold until verification is complete. Taxpayers must e-verify within 30 days from the date of filing using Aadhaar OTP, net banking, Demat account, or by sending a signed physical copy of ITR-V to CPC Bengaluru. E-verification confirms the authenticity of your filing and completes the compliance cycle.

Ignoring Latest Income Tax Updates

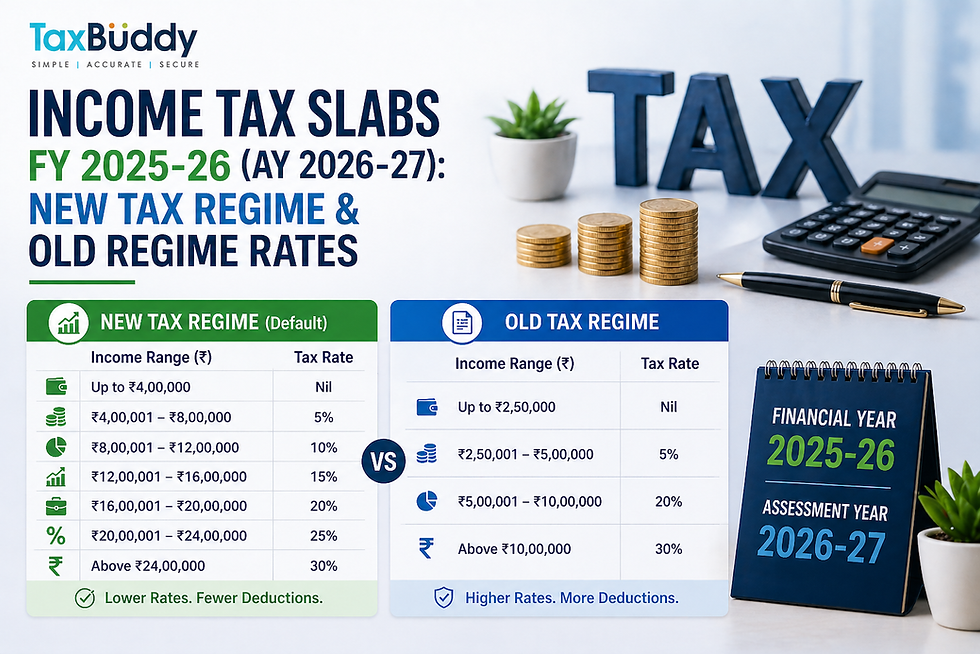

Each financial year brings updates through the Union Budget or CBDT notifications that impact tax rates, exemptions, and filing procedures. For FY 2024–25, Budget 2025 introduced revised tax slabs, updated standard deductions, and simplified TDS reporting requirements. Not being aware of such changes may result in misreporting or missed benefits. Always review official updates or rely on credible platforms like TaxBuddy, which automatically integrates the latest rules into your filing process.

Missing Foreign Income and Capital Gains Reporting

Taxpayers earning from foreign assets, stocks, or overseas employment often forget to disclose global income or capital gains. Such omissions can lead to severe penalties under the Income Tax Act and FEMA regulations. Similarly, capital gains from property, mutual funds, or shares must be reported using the correct ITR form—typically ITR-2. Maintaining supporting documents such as purchase and sale statements ensures transparency and accuracy in reporting.

Errors in PAN-Aadhaar or Bank Linking

Incorrect or incomplete linking between PAN, Aadhaar, and bank accounts can disrupt refund processing and generate mismatch notices. The Income Tax Department has made PAN-Aadhaar linkage mandatory for all taxpayers. Before filing, verify linkage status on the e-filing portal and correct discrepancies through the UIDAI website or your bank branch. Failure to link may render your PAN inoperative, restricting tax-related transactions.

Filing ITR After the Due Date

Missing the ITR filing deadline not only attracts a penalty under Section 234F but also results in loss of certain deductions and delayed refunds. Late filing may also prevent you from carrying forward losses for future tax adjustments. To avoid last-minute errors, complete your return and verification well before the due date. Filing early gives ample time to rectify discrepancies and ensures timely refund credit.

TaxBuddy Mobile App for Simplified ITR Filing

TaxBuddy simplifies the entire ITR filing process by combining automation with expert guidance. The app auto-fills data from Form 16, Form 26AS, and AIS, reducing manual errors. It validates deductions, highlights mismatches, and helps users choose the correct ITR form. Instant e-verification and refund tracking make filing faster and stress-free.

Conclusion

Accuracy is the foundation of smooth ITR filing in 2025. Small mistakes—such as wrong forms, unverified returns, or missed income disclosures—can lead to notices, penalties, and refund delays. Staying updated with the latest tax changes and using AI-enabled tools ensures precision and compliance. TaxBuddy’s intelligent platform combines automation with expert review, empowering taxpayers to file with confidence and avoid common pitfalls that can otherwise disrupt financial planning. For anyone looking for assistance in tax filing, it is highly recommended to download the TaxBuddy mobile app for a simplified, secure, and hassle-free experience.

FAQs

Q1. Does TaxBuddy offer both self-filing and expert-assisted plans for ITR filing, or only expert-assisted options?

TaxBuddy offers both self-filing and expert-assisted plans to suit different taxpayers’ needs. The self-filing plan is ideal for salaried individuals with simple income structures, allowing users to upload Form 16, auto-fill data, and file independently using AI-driven tools. The expert-assisted plan is designed for those with complex returns involving capital gains, business income, or multiple sources. In this plan, qualified tax experts handle review, computation, and filing, ensuring compliance and accuracy while minimizing the risk of errors or notices.

Q2. Which is the best site to file ITR?

The official e-filing portal of the Income Tax Department (incometax.gov.in) is the statutory platform for filing returns. However, platforms like TaxBuddy have made filing more convenient by simplifying the process through automation and expert guidance. TaxBuddy’s AI-driven system ensures error-free filings, automatic data import from Form 16 and 26AS, and instant e-verification. The platform also offers real-time expert support, making it one of the best options for those seeking a smooth and secure ITR filing experience.

Q3. Where to file an income tax return?

Income tax returns can be filed either through the official government portal (incometax.gov.in) or via authorized platforms such as TaxBuddy. TaxBuddy provides an integrated filing experience where users can submit their ITR online, verify details, calculate taxes automatically, and track refunds. The platform syncs with government databases to ensure accurate pre-filled information and smooth submission without the need for manual entry.

Q4. What if the wrong ITR form is used?

Using an incorrect ITR form results in your return being marked defective under Section 139(9) of the Income Tax Act. The taxpayer will receive a notice to file the correct form within a specified period. If the correction is not made in time, the return is treated as invalid, meaning it will be considered as not filed at all. This may lead to penalties, loss of refund eligibility, or interest liabilities. TaxBuddy automatically recommends the correct form based on income type and category, reducing such risks.

Q5. How to ensure AIS and Form 26AS match correctly?

To ensure accuracy, download both the Annual Information Statement (AIS) and Form 26AS from the Income Tax portal. Compare all reported entries such as salary income, interest from banks, dividend income, and TDS details. If discrepancies arise—say, if a TDS credit is missing or income appears inflated—contact the deductor (employer, bank, or payer) to correct it. TaxBuddy’s system automatically cross-verifies this data and alerts users about mismatches before filing, ensuring consistent and correct reporting.

Q6. Can false deduction claims attract penalties?

Yes. Claiming deductions without valid proof or claiming ineligible deductions can result in penalties under Section 270A for underreporting or misreporting of income. The taxpayer may face a penalty of up to 50% of the tax due on understated income. In severe cases, prosecution may also apply. Keeping original receipts, certificates, and investment proofs is essential. Platforms like TaxBuddy flag potential deduction errors and ensure only valid claims are made, protecting you from unnecessary scrutiny.

Q7. What if ITR is not e-verified within 30 days?

If the ITR is not e-verified within 30 days of filing, it will be considered invalid. An unverified return is treated as if it was never filed, and any refund claim becomes void. You may then have to refile the return, possibly attracting late fees under Section 234F. Verification can be done easily using Aadhaar OTP, net banking, Demat account, or through the TaxBuddy app, which provides instant e-verification options to complete the filing process.

Q8. How to report capital gains accurately in 2025?

Capital gains from the sale of property, mutual funds, or shares must be reported under the appropriate ITR form, generally ITR-2. Different tax rates apply based on the holding period and asset type—short-term and long-term gains are treated separately. Supporting documents like purchase price, sale value, and brokerage charges should be maintained. TaxBuddy’s automated calculator categorizes gains correctly and computes tax liability as per the latest 2025 regulations, ensuring full compliance.

Q9. How to link PAN and Aadhaar for ITR filing?

PAN and Aadhaar linkage is mandatory for filing income tax returns. To link them, visit the e-filing portal (incometax.gov.in), log in, and select “Link Aadhaar” under your profile settings. Enter your Aadhaar number, verify details, and confirm using OTP. If your details don’t match, update them through the UIDAI website or respective authority. Once linked successfully, your PAN becomes active for all tax purposes. TaxBuddy reminds users to complete this step before filing to prevent submission errors or refund delays.

Q10. Can a revised ITR be filed after an error?

Yes. If an error or omission is discovered after submission, a revised return can be filed under Section 139(5) within the allowed timeframe—generally before December 31 of the assessment year or completion of assessment, whichever is earlier. The revised ITR replaces the original one and rectifies mistakes in income, deductions, or personal details. TaxBuddy’s platform helps identify discrepancies automatically and assists in filing revised returns accurately.

Q11. What penalties apply for late filing in 2025?

Under Section 234F of the Income Tax Act, a late filing penalty of ₹5,000 applies if the return is filed after the due date but before December 31 of the assessment year. For taxpayers with income below ₹5 lakh, the penalty is reduced to ₹1,000. Additionally, delayed filing may attract interest under Sections 234A, 234B, and 234C and can also result in the loss of certain deductions or carry-forward benefits. Timely filing through TaxBuddy ensures compliance and prevents such penalties.

Q12. How does TaxBuddy ensure error-free ITR filing?

TaxBuddy combines AI automation with professional expertise to deliver accurate and compliant tax filings. The system auto-imports data from Form 16, Form 26AS, and AIS, minimizing manual entry errors. It validates deduction claims, highlights mismatches, and calculates tax liability in real time. Users also have access to expert review before submission, ensuring every return is compliant and optimized. This dual-layer approach provides a seamless, error-free, and secure tax filing experience for 2025.

Comments