ITR Filing Guide for Startup Founders & Entrepreneurs

- PRITI SIRDESHMUKH

- Nov 28, 2025

- 9 min read

Filing Income Tax Returns (ITR) is a crucial responsibility for every startup founder and entrepreneur in India. Even if a startup records losses or hasn’t begun generating revenue, filing ITR is mandatory under the Income Tax Act, 1961. It helps establish financial credibility, ensures compliance, and enables startups to carry forward losses for future tax benefits. With updated rules under Budget 2025 and simplified e-filing procedures, startups can now manage tax filing more efficiently using platforms like TaxBuddy, which offer automation and expert support for accurate submissions.

Table of Contents

Importance of ITR Filing for Startup Founders & Entrepreneurs

Who Needs to File ITR in a Startup?

Choosing the Correct ITR Form for Startups

Step-by-Step Process of ITR Filing for Startups

Understanding Tax Deductions and Benefits under Section 80-IAC

Compliance Deadlines and Late Filing Penalties

Common Filing Errors Made by Startup Founders

ITR Filing for LLPs, Partnerships, and Private Limited Companies

How TaxBuddy Simplifies Startup ITR Filing

Documents Required for ITR Filing by Startups

Maintaining Bank Account Records and KYC for Startups

Conclusion

FAQs

Importance of ITR Filing for Startup Founders & Entrepreneurs

Income Tax Return (ITR) filing is one of the most critical compliance responsibilities for startup founders and entrepreneurs. It not only fulfills the legal obligation under the Income Tax Act, 1961, but also serves as a reflection of the company’s transparency and credibility. Regular ITR filing helps startups maintain clean financial records, which are crucial for future funding, loan applications, and business expansions. Even when the startup is not generating profits, filing ITR ensures that business losses can be carried forward to offset future taxable income. Additionally, a consistent filing record builds trust with investors and government authorities, strengthening the startup’s financial standing in the long run.

Who Needs to File ITR in a Startup?

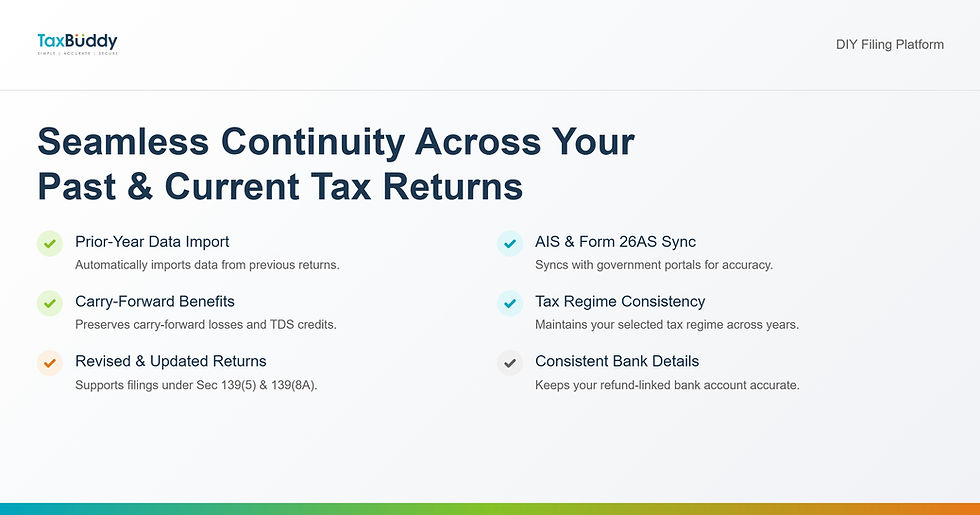

Every registered startup—whether a Private Limited Company, Limited Liability Partnership (LLP), or Partnership firm—is required to file an ITR annually, irrespective of its profit or loss status. Startup founders must also file individual ITRs if their total personal income exceeds the basic exemption limit. This includes income from salary, business profits, capital gains, or freelancing. Even early-stage startups with zero revenue or minimal activity must file returns to maintain compliance and preserve eligibility for tax benefits like the Section 80-IAC exemption. Non-filing can lead to penalties, loss of carry-forward benefits, and difficulties in securing financial credibility.

Choosing the Correct ITR Form for Startups

Selecting the right ITR form is crucial to ensure correct reporting and avoid notices from the Income Tax Department.

ITR-6: Applicable to Private Limited Companies, excluding those claiming exemptions under Section 11.

ITR-5: Used by LLPs and Partnership firms.

ITR-1 (Sahaj) or ITR-2: Suitable for individual founders, depending on their income type. Choosing the wrong form may lead to rejection of the return or trigger scrutiny. Therefore, understanding the nature of the business structure before filing is essential for accurate reporting and compliance.

Step-by-Step Process of ITR Filing for Startups

Organize Financial Data – Collect income statements, expense invoices, bank statements, and supporting records for the financial year.

Calculate Taxable Income – Deduct eligible business expenses, depreciation, and deductions like Section 80-IAC.

Pay Pending Taxes – Adjust for TDS and advance tax payments. Pay any remaining self-assessment tax before filing.

Prepare and Upload ITR – Use the Income Tax e-filing portal or a platform like TaxBuddy to upload details and documents accurately.

Verify ITR – Complete verification using Aadhaar OTP, EVC, or Digital Signature Certificate (DSC).

Keep Acknowledgment Copy – Save the acknowledgment for audit, loan, or investor reference.

Following these steps ensures a complete and error-free filing experience while reducing the risk of late filing penalties or departmental scrutiny.

Understanding Tax Deductions and Benefits under Section 80-IAC

Section 80-IAC offers a major tax incentive for eligible startups registered under the Department for Promotion of Industry and Internal Trade (DPIIT). It allows 100% tax exemption on profits for any three consecutive years out of the first ten years since incorporation. This helps startups reinvest their profits into business growth and innovation. To qualify, the startup must be incorporated as a Private Limited Company or LLP after April 1, 2016, and its annual turnover must not exceed ₹100 crore. Founders should ensure that the startup is DPIIT-recognised to avail of this benefit. Proper documentation and timely ITR filing are mandatory to claim the deduction successfully.

Compliance Deadlines and Late Filing Penalties

For the financial year 2024–25, the due date for filing ITR for startups subject to audit is 31st October 2025. Delayed filing can result in penalties under Section 234F—₹1,000 if the total income is below ₹5 lakh and ₹5,000 if it exceeds ₹5 lakh. Additionally, interest under Sections 234A, 234B, and 234C applies for the delay in tax payment. Non-compliance may also lead to the loss of carry-forward benefits of business losses and depreciation. Filing within the deadline ensures peace of mind, smoother scrutiny handling, and eligibility for government schemes or investor opportunities.

Common Filing Errors Made by Startup Founders

Selecting the wrong ITR form for the entity type.

Missing out on reporting all income sources, including bank interest or freelance income.

Failing to reconcile GST returns with financial statements.

Ignoring TDS mismatches or discrepancies in Form 26AS and AIS.

Missing the e-verification step after filing, which invalidates the return.

Forgetting to claim eligible deductions under Section 80-IAC or startup-related exemptions. Avoiding these common mistakes ensures the startup remains compliant and avoids unnecessary notices or penalties.

ITR Filing for LLPs, Partnerships, and Private Limited Companies

Different business structures have distinct filing requirements:

LLPs must file ITR-5 along with Form 3CA/3CB and Form 3CD if audit requirements apply.

Partnership firms also file ITR-5 and must include partner remuneration and interest details as per the partnership deed.

Private Limited Companies use ITR-6 and are required to get their accounts audited under Section 44AB if turnover exceeds ₹1 crore (or ₹10 crore if 95% of transactions are digital). Each entity must ensure compliance with relevant provisions, including maintaining proper accounting books, GST filings, and TDS returns, as they form the basis of ITR accuracy.

How TaxBuddy Simplifies Startup ITR Filing

TaxBuddy offers an AI-driven tax filing solution designed to simplify the ITR process for startups and entrepreneurs. It automates data extraction from documents like PAN, Aadhaar, and Form 16, minimizing manual errors. The platform supports both self-filing and expert-assisted options—startups can choose to file independently with guided automation or connect with certified tax experts for professional support. TaxBuddy also ensures accurate selection of ITR forms, compliance with updated rules, and real-time error checks. Its post-filing support helps address notices or queries, making it a complete solution for startups aiming for seamless compliance and peace of mind.

Documents Required for ITR Filing by Startups

PAN card and incorporation certificate

Bank account statements for the financial year

Profit & Loss statement and Balance Sheet

GST returns and TDS certificates

Form 26AS and AIS reports

Audit report (if applicable)

Partner or shareholder details

Startup recognition certificate under DPIIT (if claiming Section 80-IAC) Having these documents ready ensures accuracy in income computation, deduction claims, and audit verification.

Maintaining Bank Account Records and KYC for Startups

Bank account KYC and maintenance are essential for financial compliance. Founders must ensure that startup bank accounts are opened with accurate details such as PAN, GST registration, and incorporation documents. The account opening forms must include authorized signatories, business address proof, and the nature of the business. Consistency in financial data across bank accounts, GST filings, and ITR submissions prevents reconciliation errors and scrutiny. Maintaining proper KYC records also helps during audits, investment due diligence, and fund transfers under regulatory frameworks.

Conclusion

Filing ITR is not merely a statutory obligation but a foundation of credibility and growth for startups. It reflects transparency, facilitates funding, and ensures eligibility for government incentives and deductions. With evolving compliance requirements, startup founders can benefit from using intelligent tax platforms that simplify the filing journey. For anyone looking for assistance in tax filing, it is highly recommended to download theTaxBuddy mobile app for a simplified, secure, and hassle-free experience.

FAQs

Q1. Does TaxBuddy offer both self-filing and expert-assisted plans for ITR filing, or only expert-assisted options? TaxBuddy provides both self-filing and expert-assisted ITR filing options, catering to different types of taxpayers. The self-filing plan is AI-driven, designed for users who prefer to handle their own filings but still want automation and error detection features. It pre-fills data from PAN, Aadhaar, and Form 16 to reduce manual effort. The expert-assisted plan, on the other hand, connects users with certified tax professionals who review, prepare, and file the return on their behalf. This plan is ideal for complex filings such as startups, companies, or individuals with multiple income sources, ensuring accuracy and complete compliance.

Q2. Which is the best site to file ITR? The official Income Tax Department portal (www.incometax.gov.in) is the statutory platform for filing all income tax returns in India. However, for startups and entrepreneurs looking for a simpler and more intuitive experience, platforms like TaxBuddy stand out. TaxBuddy offers automated data entry, built-in compliance checks, and expert review options. It helps users avoid errors, ensures timely filing, and provides post-filing assistance for issues like notices or discrepancies. For startups handling multiple accounts and deductions, this ease of use and professional support make TaxBuddy one of the best ITR filing platforms in India.

Q3. Where to file an income tax return? Income tax returns can be filed online through the government’s e-filing portal (www.incometax.gov.in) or through trusted private platforms like TaxBuddy. Filing through TaxBuddy provides additional benefits such as real-time error detection, AI-assisted computation, and access to experts who handle filing from start to finish. Whether you’re a startup founder, a freelancer, or a business owner, using such platforms ensures accuracy and compliance with the latest tax laws.

Q4. Is ITR filing mandatory for startups? Yes, ITR filing is mandatory for all registered startups in India, even if the business has not generated revenue or is incurring losses. Filing returns helps maintain legal compliance under the Income Tax Act, 1961, and allows startups to carry forward losses to offset future profits. It also plays a vital role in establishing the financial credibility of the business, which is crucial for securing funding, loans, and government benefits. Startups that skip filing can face penalties and lose valuable tax benefits.

Q5. Which ITR form should startup founders use? The applicable ITR form depends on the startup’s structure and the founder’s income type:

ITR-6: For Private Limited Companies, excluding those claiming exemptions under Section 11.

ITR-5: For LLPs and Partnership firms.

ITR-1 or ITR-2: For individual founders, depending on whether income comes from salary, capital gains, or business. Filing with the wrong form may result in rejection or notices. TaxBuddy’s automated system ensures the correct ITR form is selected based on entity type and income classification.

Q6. What tax exemptions are available under Section 80-IAC? Section 80-IAC of the Income Tax Act provides a 100% tax exemption on profits for three consecutive years within the first ten years of incorporation to eligible startups. To qualify, the startup must be recognised by the Department for Promotion of Industry and Internal Trade (DPIIT), incorporated after April 1, 2016, and have a turnover not exceeding ₹100 crore in any financial year. This benefit helps startups reinvest profits into growth. Claiming this deduction requires proper documentation and timely ITR filing.

Q7. Can a startup correct errors in a filed return? Yes, startups can file a revised return under Section 139(5) if they identify errors or omissions after submitting the original ITR. The revised return can be filed within 12 months from the end of the relevant assessment year or before the assessment is completed, whichever is earlier. It’s important to verify the revised ITR just like the original return. Platforms like TaxBuddy help identify discrepancies and guide startups through the correction process to avoid future scrutiny.

Q8. What are the penalties for late filing? If a startup fails to file its ITR by the due date, it becomes liable for penalties under Section 234F. The penalty is ₹1,000 if the total income is below ₹5 lakh and ₹5,000 if it exceeds ₹5 lakh. Additionally, interest under Sections 234A, 234B, and 234C applies for delays in tax payment. Non-filing also results in loss of carry-forward benefits of business losses or unabsorbed depreciation. Filing on time ensures legal compliance and protects the startup’s eligibility for future deductions.

Q9. What documents are required for ITR filing by startups? Startups should keep the following documents ready before filing ITR:

PAN card and Certificate of Incorporation

Bank statements for the financial year

Profit & Loss statement and Balance Sheet

GST returns and TDS certificates

Form 26AS and Annual Information Statement (AIS)

Audit report, if applicable

Startup recognition certificate from DPIIT (for Section 80-IAC claims) Maintaining these documents ensures accurate filing, smooth verification, and readiness for audit or investor scrutiny.

Q10. How does ITR filing help startups attract investors? Timely and accurate ITR filing enhances a startup’s financial transparency, a critical factor for investors. It reflects responsible governance and compliance, making it easier to pass due diligence checks during funding rounds. Investors often request past ITRs to analyze revenue growth, expense management, and tax discipline. A startup with consistent ITR filings stands out as reliable and investment-worthy. Filing through professional platforms like TaxBuddy further strengthens this image by ensuring accuracy and regulatory adherence.

Q11. What if the ITR is not verified after filing? An unverified ITR is treated as invalid by the Income Tax Department. Verification confirms the authenticity of the return and must be done within 30 days of filing using any of the following methods: Aadhaar OTP, Electronic Verification Code (EVC), or Digital Signature Certificate (DSC). Failure to verify can nullify the filing, requiring the startup to refile the return. TaxBuddy ensures this crucial step is completed, reducing the risk of invalidation or delays in processing.

Q12. Can losses be carried forward if the return is filed late? No. Under the Income Tax Act, the carry-forward of business losses is allowed only if the ITR is filed before the due date specified under Section 139(1). Filing after the deadline forfeits this benefit, meaning the startup cannot use previous losses to offset future profits. To preserve these advantages, it is vital for founders to file their returns on time. TaxBuddy’s system reminders and expert support help startups meet all filing timelines and maintain eligibility for loss carry-forward provisions.

Comments