Using Form 15G or Form 15H to Avoid TDS on PF Withdrawal

- CA Pratik Bharda

- Apr 14

- 9 min read

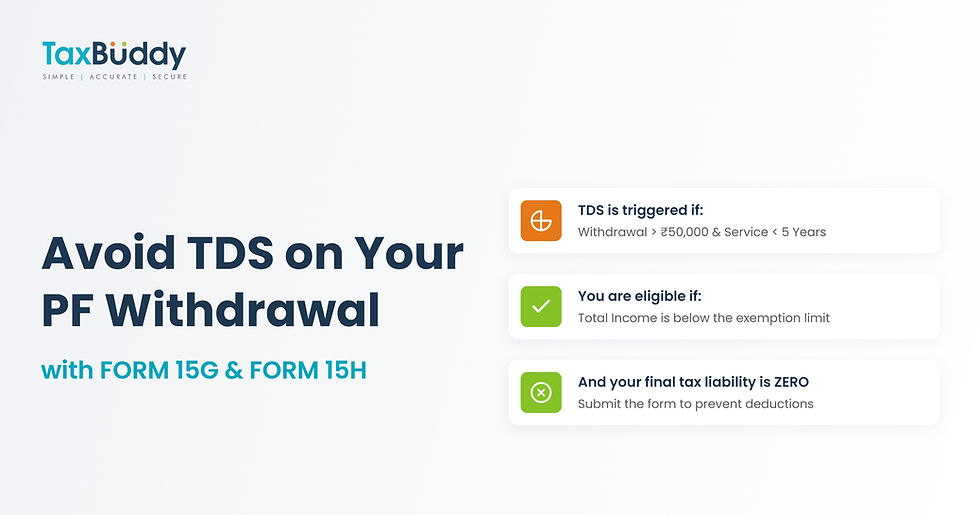

Form 15G and Form 15H are commonly used declarations under the Income Tax Act, 1961, to avoid TDS on certain incomes, including PF withdrawals, when the taxpayer’s total income is below the basic exemption limit, and tax liability is zero. TDS on PF withdrawal is triggered when the withdrawal exceeds ₹50,000, and the service is less than five years. In such cases, submitting the correct form helps prevent unnecessary tax deductions and improves cash flow. Understanding eligibility, conditions, and proper submission is essential to ensure compliance and avoid future tax issues.

Using Form 15G or Form 15H allows eligible individuals to avoid TDS on PF withdrawal by declaring that their total income for the financial year is below the taxable limit and that no tax is payable, provided the withdrawal conditions under Section 192A are met.

Table of Contents

Eligibility Criteria to Use Form 15G or Form 15H for PF Withdrawal

Step-by-Step Process to Submit Form 15G or Form 15H for PF Withdrawal

Is TDS Avoidance on PF Withdrawal Allowed in the New Tax Regime

What Happens If Form 15G or Form 15H Is Submitted Incorrectly

Can You Claim a Refund If TDS Is Already Deducted on PF Withdrawal

How Digital Platforms Simplify TDS Management and Tax Filing

What are Form 15G and Form 15H Under Income Tax Act?

Form 15G and Form 15H are self-declaration forms under Section 197A of the Income Tax Act, 1961. These forms allow eligible taxpayers to request that no tax be deducted at source on certain incomes if their total tax liability for the financial year is zero.

Form 15G is applicable to resident individuals below 60 years of age and Hindu Undivided Families, while Form 15H is meant for resident individuals aged 60 years or above. These forms are commonly used to avoid TDS on interest income, fixed deposits, and PF withdrawals where applicable.

The purpose of these forms is to prevent unnecessary deduction of tax when the taxpayer is not liable to pay income tax.

Legal Basis for TDS on PF Withdrawal Under Section 192A

TDS on Provident Fund withdrawal is governed by Section 192A of the Income Tax Act, introduced to ensure tax compliance on premature withdrawals.

Under this provision, TDS at 10 per cent is deducted when the withdrawal amount exceeds ₹50,000, and the employee has not completed five years of continuous service. This applies to both employer and employee contributions, along with interest earned.

The provision ensures that taxable withdrawals are captured within the tax system, while still allowing eligible individuals to avoid TDS through proper declarations.

When TDS Applies to PF Withdrawal

TDS on PF withdrawal is applicable only under specific conditions.

It is triggered when the total withdrawal exceeds ₹50,000, and the employee has completed less than five years of continuous service. If both conditions are satisfied, TDS is deducted at the prescribed rate.

If the service period is five years or more, the withdrawal is generally tax-free, and no TDS is applicable. Similarly, if the withdrawal amount is ₹50,000 or less, TDS is not deducted even if the service period is shorter.

Understanding these thresholds is important before deciding whether to submit Form 15G or Form 15H.

Eligibility Criteria to Use Form 15G or Form 15H for PF Withdrawal

To use Form 15G or Form 15H for PF withdrawal, certain conditions must be met.

The individual must be a resident taxpayer. The total estimated income for the financial year, including PF withdrawal and other sources, should be below the basic exemption limit.

In addition, the total tax liability must be zero. Form 15G is applicable to individuals below 60 years, while Form 15H is applicable to senior citizens aged 60 years or above.

If these conditions are not satisfied, the forms cannot be used to avoid TDS.

Difference Between Form 15G and Form 15H

The primary difference between Form 15G and Form 15H lies in eligibility.

Form 15G is meant for individuals below 60 years of age and HUFs, provided their total income is below the exemption limit and tax liability is nil.

Form 15H is specifically designed for senior citizens aged 60 years or above. Even if their income exceeds the exemption limit, they can still submit Form 15H as long as their tax liability after deductions is zero.

This distinction ensures that senior citizens have greater flexibility in avoiding TDS.

Conditions to Avoid TDS Using Form 15G or Form 15H

To successfully avoid TDS on PF withdrawal, the taxpayer must satisfy all required conditions.

The total income must be below the basic exemption limit, and the overall tax liability must be zero after considering deductions.

The PF withdrawal should meet the conditions where TDS would otherwise apply, such as withdrawal exceeding ₹50,000 with less than five years of service.

The declaration must be accurate and supported by valid PAN details. Incorrect declarations can lead to penalties.

Step-by-Step Process to Submit Form 15G or Form 15H for PF Withdrawal

The process begins with estimating total income for the financial year to confirm eligibility.

The correct form must be selected based on age. Form 15G is used by individuals below 60 years, while Form 15H is used by senior citizens.

The form must be filled with accurate details, including PAN, income estimate, and declaration of nil tax liability.

It is then submitted along with the PF withdrawal application through the EPFO portal or the employer system, depending on the process followed.

Once accepted, TDS is not deducted from the withdrawal amount.

Documents Required for Form 15G or Form 15H Submission

Certain documents are required to support the declaration.

These include PAN card, identity proof, PF account details, and income estimates. In some cases, supporting documents for deductions may also be required.

Providing accurate and complete documentation helps ensure smooth processing and avoids rejection of the declaration.

Role of PAN in Avoiding TDS on PF Withdrawal

PAN plays a critical role in the submission of Form 15G or Form 15H.

Without a valid PAN, the declaration may not be accepted, and TDS may be deducted at a higher rate as per tax rules.

PAN ensures proper tracking of income and helps link the declaration to the taxpayer’s records. It also enables accurate reporting in Form 26AS and AIS.

Is TDS Avoidance on PF Withdrawal Allowed in the New Tax Regime

TDS avoidance through Form 15G or Form 15H is allowed irrespective of the tax regime chosen.

The eligibility depends on total income and tax liability, not on whether the taxpayer opts for the new or old tax regime.

However, under the new tax regime, fewer deductions are available, which may affect the calculation of total income and eligibility for submitting these forms.

How PF Withdrawal Taxation Works in the Old Tax Regime

Under the old tax regime, PF withdrawal is taxed if the employee has not completed five years of continuous service.

The withdrawn amount is added to the total income and taxed according to applicable slab rates. However, deductions under sections such as 80C and 80D can reduce taxable income.

If the total income after deductions falls below the exemption limit, Form 15G or Form 15H can be used to avoid TDS.

Common Mistakes While Using Form 15G or Form 15H

One common mistake is underestimating total income and submitting the form even when tax liability exists.

Another error is providing incorrect PAN details or incomplete information in the form.

Some taxpayers submit the form without checking eligibility conditions, which can lead to compliance issues later.

Avoiding these mistakes is important for accurate tax reporting.

What Happens If Form 15G or Form 15H Is Submitted Incorrectly

If the form is submitted incorrectly or with false information, the taxpayer may face consequences.

Tax authorities may treat it as misrepresentation, and the taxpayer may be required to pay the applicable tax along with interest and penalties.

The deductor may also reject the form if the information provided is incomplete or incorrect.

Can You Claim a Refund If TDS Is Already Deducted on PF Withdrawal

If TDS has already been deducted and the taxpayer’s total income is below the exemption limit, a refund can be claimed.

This is done by filing an income tax return and reporting the TDS deducted.

After processing the return, the Income Tax Department refunds the excess tax paid.

Practical Scenarios for Using Form 15G or Form 15H

In situations where an individual withdraws PF before completing five years of service but has a low total income, Form 15G can be used to avoid TDS.

Senior citizens withdrawing PF with minimal income can use Form 15H.

In cases where additional income, such as interest or rental income, exists, total income must be evaluated carefully before submitting the form.

These scenarios highlight the importance of proper planning.

How Digital Platforms Simplify TDS Management and Tax Filing

Digital platforms help simplify the process of managing TDS and tax compliance.

They allow taxpayers to estimate total income, check eligibility for Form 15G or Form 15H, and track deductions.

Platforms like TaxBuddy assist in filing income tax returns, managing TDS records, and ensuring compliance with tax laws.

This reduces errors and improves efficiency in tax management.

Conclusion

Using Form 15G or Form 15H to avoid TDS on PF withdrawal can be beneficial when eligibility conditions are met. Accurate estimation of income, correct submission of forms, and proper documentation are essential to ensure compliance and avoid future tax liabilities. Since PF withdrawals, TDS rules, and tax calculations can be complex, using digital tools can simplify the process and reduce errors. For anyone looking for assistance in tax filing, it is highly recommended to download the TaxBuddy mobile app for a simplified, secure, and hassle-free experience.

FAQs

Q1. Can Form 15G or Form 15H completely eliminate TDS on PF withdrawal?

Yes, Form 15G or Form 15H can help avoid TDS on PF withdrawal, but only if all conditions are satisfied. The individual’s total income for the financial year must be below the basic exemption limit, and the total tax liability must be zero. If these conditions are not met, TDS cannot be avoided.

Q2. Is Form 15G applicable if the PF withdrawal is less than ₹50,000?

No, Form 15G or Form 15H is generally not required if the PF withdrawal amount is ₹50,000 or less. In such cases, TDS is not applicable even if the employee has not completed five years of service.

Q3. Can Form 15H be submitted even if income exceeds the basic exemption limit?

Yes, senior citizens can submit Form 15H even if their total income exceeds the basic exemption limit, provided their final tax liability after deductions is zero. This flexibility is specific to Form 15H.

Q4. Can Form 15G or Form 15H be used if the PF withdrawal is after five years of service?

If PF withdrawal is made after completing five continuous years of service, it is generally tax-free. In such cases, TDS does not apply, and there is usually no need to submit Form 15G or Form 15H.

Q5. What income should be considered while submitting Form 15G or Form 15H?

All sources of income must be considered, including salary, interest income, rental income, capital gains, and PF withdrawal. The declaration should be based on the total estimated income for the financial year, not just the PF withdrawal.

Q6. Is it mandatory to submit Form 15G or Form 15H for PF withdrawal?

No, it is not mandatory. These forms are only required if the individual wants to avoid TDS on PF withdrawal, where TDS would otherwise be applicable.

Q7. Can Form 15G be submitted if there is income from multiple sources?

Yes, Form 15G can be submitted even if there are multiple income sources, but only if the total income from all sources remains below the exemption limit and the tax liability is zero.

Q8. What happens if Form 15G or Form 15H is rejected by the EPFO?

If the form is rejected due to incorrect or incomplete details, TDS may be deducted on the PF withdrawal. The individual can later claim a refund by filing an income tax return if eligible.

Q9. Can Form 15G or Form 15H be revised after submission?

Once submitted, the form generally cannot be revised for that specific transaction. However, if incorrect information was provided, the taxpayer must ensure correct reporting while filing the income tax return.

Q10. Is online submission of Form 15G or Form 15H available for PF withdrawal?

Yes, many EPFO and employer portals allow online submission of Form 15G or Form 15H along with the PF withdrawal application. This simplifies the process and reduces paperwork.

Q11. Will submitting Form 15G or Form 15H exempt the income from tax?

No, these forms only prevent TDS deduction. If the income is actually taxable based on total income, the taxpayer must still pay the applicable tax while filing the income tax return.

Q12. How can taxpayers ensure the correct use of Form 15G or Form 15H?

Taxpayers should carefully estimate their total annual income, verify eligibility conditions, and provide accurate details in the form. Keeping track of all income sources and deductions helps ensure that the declaration is valid and avoids future tax issues.

Comments