Section 80EEB: Deduction on Electric Vehicle Loan Interest (AY 2025-26)

- Nimisha Panda

- Jul 25, 2025

- 12 min read

The section 80EEB deduction provides a tax benefit on the interest paid for an Electric Vehicle (EV) loan under the Income Tax Act. It's important for taxpayers to understand its current status for the Assessment Year 2025-26. While new loans sanctioned after March 31, 2023, are not eligible for this 80eeb deduction, individuals who secured their EV loans within the specified window (April 1, 2019, to March 31, 2023) can still claim this electric vehicle tax benefit. This article explains the eligibility criteria, the deduction amount, how you can claim it when filing your Income Tax Return, the necessary documents, and how 80eeb income tax rules apply under different tax regimes.

Table of content

What is Section 80EEB of the Income Tax Act?

Section 80EEB of the Income Tax Act, 1961, was introduced to encourage people to buy electric vehicles. This section offers a tax deduction on the interest part of a loan taken to purchase an electric vehicle. The Finance Act, 2019, brought this provision into effect from Assessment Year 2020-21. The primary aim of what is section 80eeb was to promote a cleaner environment by making electric vehicles more affordable.

The 80eeb of income tax act allows individuals to reduce their taxable income by the amount of interest on EV loan paid, subject to certain limits. This initiative made switching to electric mobility a more attractive option for many taxpayers. Understanding 80eeb explained in detail can help eligible individuals maximize their tax savings.

Current Status of Section 80EEB: Key Dates to Remember

Understanding the section 80eeb applicability hinges on some crucial dates. The government introduced this deduction for a specific period to boost EV adoption. For anyone wondering, "is 80eeb still available?", the answer depends on when the EV loan was sanctioned.

Here are the key points regarding the 80eeb last date and its availability for AY 2025-26:

The loan for the electric vehicle must have been sanctioned between April 1, 2019, and March 31, 2023.

No deduction under Section 80EEB is available for EV loans sanctioned on or after April 1, 2023.

If your loan was sanctioned within the eligible timeframe (between April 1, 2019, and March 31, 2023), you can continue to claim the deduction on the interest paid each year. This claim is valid until the loan is fully repaid. So, for 80eeb for ay 2025-26, if you meet this condition, you can claim the benefit.

Who is Eligible to Claim Deduction Under Section 80EEB?

The 80eeb eligibility criteria are quite specific. Taxpayers need to meet certain conditions to claim this deduction for an electric vehicle loan. Not everyone who buys an EV can automatically get this tax break.

Here are the main conditions for 80EEB:

Taxpayer Type: Only Individuals can claim the deduction under Section 80EEB. This benefit is not available for a Hindu Undivided Family (HUF), Association of Persons (AOP), Body of Individuals (BOI), company, or any other type of taxpayer. So, it's specifically an 80eeb for individuals.

Loan Purpose: The loan must be taken specifically for the purchase of an Electric Vehicle. This means the funds should be directly used for acquiring an EV.

Loan Source: The loan must come from a financial institution, which includes a bank or a banking institution governed by the Banking Regulation Act, 1949, or a specified non-banking financial company (NBFC). These NBFCs can be deposit-taking or certain non-deposit-taking ones.

Vehicle Type: The deduction applies to the purchase of a new electric vehicle. It does not cover second-hand or used EVs. The vehicle can be a two-wheeler or a four-wheeler.

It’s good to remember these points to see if you qualify. The focus is clearly on individual taxpayers buying new electric vehicles through recognized lenders.

What is an "Electric Vehicle" for Section 80EEB?

For the purpose of Section 80EEB, the term "Electric Vehicle" has a specific meaning. Not every vehicle that uses electricity might fit the electric vehicle definition for 80EEB. It's quite precise to ensure the benefit goes to genuinely eco-friendly options.

An eligible EV for 80EEB is defined as follows:

It must be a vehicle powered exclusively by an electric motor.

Its traction energy must be supplied solely by a traction battery installed in the vehicle.

The vehicle needs to have an electric regenerative braking system. This system converts the vehicle's kinetic energy into electrical energy during braking, which helps recharge the battery a bit.

So, the vehicle should rely entirely on its electric motor and battery for movement and incorporate technology like regenerative braking.

Amount of Deduction Available Under Section 80EEB

The 80EEB deduction limit specifies how much an individual can claim against the interest paid on an electric vehicle loan. The 80EEB amount is capped to ensure the benefit is reasonably distributed.

Here’s how the maximum deduction 80EEB works:

You can claim the actual interest paid on the EV loan during the financial year, OR

Rs. 1,50,000. Whichever of these two amounts is lower is the deduction you can get.

It's important to note that there's no cap on the total loan amount itself for this section, but the 80eeb interest limit for deduction purposes is fixed at Rs. 1,50,000 per financial year. This deduction is also over and above any depreciation benefits if the electric vehicle is used for business purposes.

Section 80EEB and Business Use of Electric Vehicle

If an individual uses an electric vehicle for business purposes, the 80EEB for business use rules offer some clarity. The Rs. 1,50,000 deduction under Section 80EEB on interest can still be claimed by the individual owner.

Now, what if the actual interest paid on the EV loan is more than Rs. 1,50,000? In such cases, the excess interest amount (the amount over Rs. 1,50,000) may be claimable as a business expense. This is possible if the vehicle is registered in the name of the owner or their business and is genuinely used for business activities. This claim would fall under the general rules for business expense deductions, like those in Section 37 of the Income Tax Act. It's not an extension of the 80EEB limit itself but a separate potential claim under business income.

Additionally, depreciation on the electric vehicle can also be claimed as a business expense if it's used for the business. It's always a good idea to consult a tax advisor for specific guidance on claiming EV loan interest business expense and depreciation, just to make sure everything is done correctly.

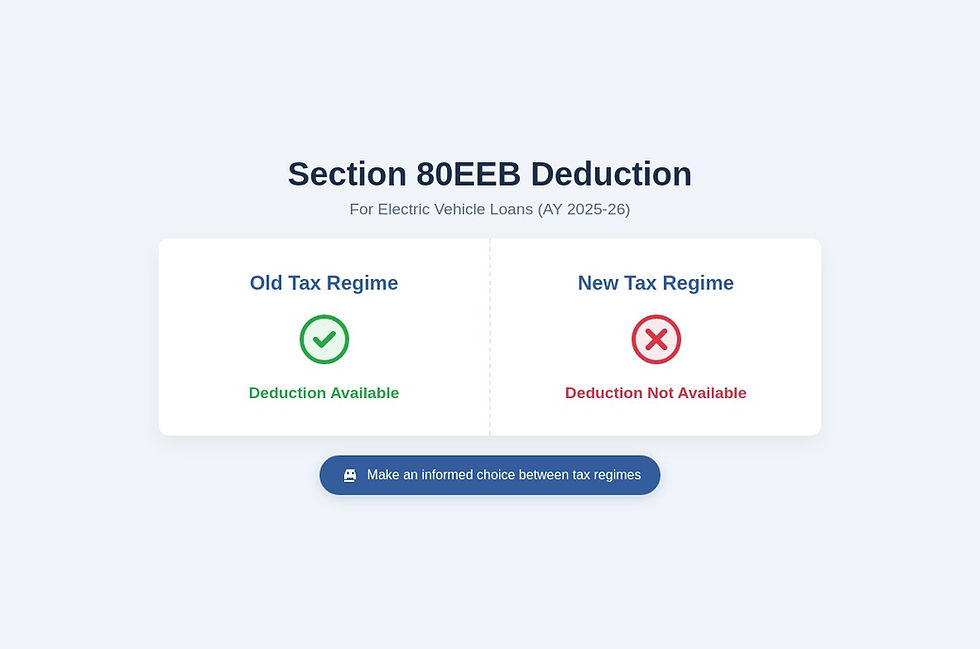

Section 80EEB Deduction: Old Tax Regime vs. New Tax Regime (AY 2025-26)

A very important point for taxpayers claiming the 80EEB deduction for Assessment Year 2025-26 is its availability under the Old Tax Regime vs. New Tax Regime. The choice of tax regime significantly impacts whether you can claim this benefit.

The Section 80EEB deduction is available only if you choose to file your taxes under the Old Tax Regime. It is NOT available if you opt for the New Tax Regime (under Section 115BAC), which is now the default regime. The new tax regime generally offers lower tax rates but does not allow many common deductions and exemptions, including the 80eeb new tax regime benefit. This is a key reason why many deductions, like 80eeb old tax regime claims, are disallowed under the new structure.

For AY 2025-26, individuals (unless they have business income and have exercised their option in a particular way previously) usually have the option to choose between the old and new regimes each year. It's vital to evaluate which regime is more beneficial after considering all eligible deductions.

Here’s a simple comparison:

Feature | Old Tax Regime | New Tax Regime (u/s 115BAC) |

Section 80EEB | Available (up to Rs. 1.5L) | Not Available |

Tax Rates | Higher, with more slabs | Generally Lower, different slabs |

Other Deductions | Many (like 80C, 80D, HRA etc.) | Most are disallowed |

Documents Required to Claim Section 80EEB Deduction

To successfully claim the 80EEB deduction, you need to have proper documents for 80EEB as proof. These documents are crucial not just for filing your return but also for substantiating your claim if the Income Tax Department asks for proof for 80EEB. With new ITR disclosure norms, having these 80eeb claim documents organized is more important than ever.

Here's a list of essential documents:

Interest Paid Certificate: This must be from the bank or NBFC that provided the loan. It should clearly show the breakup of principal and interest amounts paid during the financial year.

Loan Sanction Letter: This letter from the financial institution is proof that the loan was taken for purchasing an electric vehicle and, very importantly, that it was sanctioned between April 1, 2019, and March 31, 2023.

Vehicle Purchase Invoice: The original invoice for the EV purchase.

Registration Certificate (RC) of the EV: This shows you are the owner of the electric vehicle.

Loan Agreement & Repayment Schedule: Keep these for your records; they detail the terms of your loan.

Tax Invoice of Vehicle: The tax invoice related to the vehicle purchase.

PAN of the Lender: The Permanent Account Number (PAN) of the bank or NBFC that gave the loan is often required for various deductions now, including this one, as per new ITR utility requirements.

How to Claim Section 80EEB in Your Income Tax Return (ITR) for AY 2025-26 (FY 2024-25)

Knowing how to claim 80EEB in ITR correctly is essential for AY 2025-26 (Financial Year 2024-25). The process involves accurately reporting the deduction while filing your ITR. Recent ITR utilities have introduced more detailed disclosure requirements for claiming 80EEB deduction.

Here are the steps and details to keep in mind:

Opt for the Old Tax Regime: First and foremost, ensure you are choosing the Old Tax Regime when filing your income tax return. This deduction is not available under the New Tax Regime.

Locate Deduction Schedule: While filling out your applicable ITR form (like ITR-1 or ITR-2), find the schedule for deductions under Chapter VI-A.

Enter Eligible Amount: In that schedule, find Section 80EEB and enter the actual interest amount you paid during FY 2024-25, up to the maximum limit of Rs. 1,50,000.

Fulfill New ITR Disclosure Requirements: The latest ITR utilities for AY 2025-26 now ask for specific details for the 80EEB ITR form entry. You will likely need to provide:

Vehicle Registration Number

Lender's Name (Bank or NBFC)

Lender's PAN (Permanent Account Number)

Loan Account Number

Date of Loan Sanction

Total Loan Amount

Interest paid during the year

Outstanding loan balance as of March 31st of the financial year.

Keep Documents Ready: Have all supporting documents (interest certificate, loan sanction letter, RC, etc.) safely stored. You don't usually need to upload them with the ITR, but they are vital for your records and if the tax department requests them during scrutiny or processing.

Accurate 80EEB disclosure is very important due to new ITR validation rules.

Other Important Points Regarding Section 80EEB

Beyond the main rules, there are a few other 80EEB conditions and points to understand for a complete picture. These often address common questions about the 80EEB claim duration and specific situations.

Can deduction be claimed every year? Yes. If your EV loan was sanctioned between April 1, 2019, and March 31, 2023, you can claim the deduction on the interest paid for every year until the loan is fully repaid.

What about loan transfer? If you transfer your existing eligible EV loan from one financial institution to another (e.g., from Bank A to Bank B), you can generally continue to claim the deduction. The key is that the loan continues to be for the same electric vehicle, the interest is paid by the same individual, and other conditions of Section 80EEB are met.

Ownership of the EV: To keep claiming the deduction, the individual who took the loan must generally continue to own the electric vehicle. If the vehicle is sold before the loan is fully paid off, the deduction may not be allowed for the interest paid after the sale for the remaining period.

No double deduction: This is a standard income tax principle. The interest amount for which you claim a deduction under Section 80EEB cannot be claimed again as a deduction under any other section of the Income Tax Act. For example, you can't claim the same Rs. 1.5 lakh interest under both 80EEB and as a business expense (though, as discussed earlier, interest over Rs 1.5 lakh might be considered as a business expense if the EV is used for business).

Benefits of Section 80EEB: Beyond Tax Savings

The benefits of 80EEB extend further than just the direct tax savings for individuals. Understanding why section 80EEB was introduced sheds light on its broader positive impacts. The government brought in this measure primarily to encourage a shift towards cleaner transportation.

Here's a look at some wider advantages:

It actively promotes the adoption of eco-friendly electric vehicles.

This helps in reducing the overall carbon footprint and lessens our country's dependence on traditional fossil fuels.

The section supports the government's larger vision and initiatives for green mobility in India.

While not direct benefits of Section 80EEB itself, it's worth noting that EV owners also benefit from other government incentives like a reduced GST rate of 5% on electric vehicles and potential road tax exemptions or concessions in various states. These collectively make owning an EV more appealing.

Conclusion: Maximizing Your Eligible Section 80EEB Deduction

To sum up the 80EEB summary, Section 80EEB of the Income Tax Act offers a valuable tax deduction of up to Rs. 1.5 lakh on the interest paid for an electric vehicle loan. This benefit is specifically for loans sanctioned between April 1, 2019, and March 31, 2023. For individuals who are still repaying such loans, this deduction remains a significant way to reduce their tax outgo.

Key final thoughts on 80EEB to remember are that this deduction is claimable only if you opt for the Old Tax Regime.

Also, with the new ITR disclosure norms, ensuring you have accurate documentation and report all required details correctly in your tax return is absolutely vital. If you are eligible, make sure you claim this benefit accurately to optimize your tax savings. For any specific queries, it's always wise to consult with a TaxBuddy expert.

Frequently Asked Questions (FAQs) about Section 80EEB

Q1: Is Section 80EEB still applicable for AY 2025-26?

A: Yes, if your EV loan was sanctioned between April 1, 2019, and March 31, 2023, you can claim the deduction in AY 2025-26 for the interest paid in FY 2024-25, until your loan is repaid. New loans sanctioned after March 31, 2023, are not eligible.

Q2: What is the maximum deduction I can claim under Section 80EEB?

A: You can claim up to Rs. 1,50,000 or the actual interest paid, whichever is lower, per financial year.

Q3: Can I claim Section 80EEB if I opt for the new tax regime?

A: No, Section 80EEB deduction is not available if you opt for the new tax regime (u/s 115BAC). It can only be claimed under the old tax regime.

Q4: Is Section 80EEB applicable for electric scooters or two-wheelers?

A: Yes, the deduction is available for loans taken to purchase any new electric vehicle, including two-wheelers and four-wheelers.

Q5: Can a company or HUF claim deduction under Section 80EEB?

A: No, this deduction is only available to individual taxpayers. (Refer to the section on Who is Eligible to Claim Deduction Under Section 80EEB?)

Q6: Do I need to submit any proof to claim Section 80EEB?

A: Yes, you need documents like an interest payment certificate, loan sanction letter, and vehicle RC. For ITR filing, you'll need to provide specific details like vehicle registration no., lender details, etc.

Q7: Can I claim 80EEB for a second-hand electric vehicle?

A: No, the deduction under Section 80EEB is generally applicable for loans taken to purchase a new electric vehicle.

Q8: What if my total interest paid in a year is less than Rs. 1.5 lakh?

A: You can claim the actual amount of interest paid as a deduction. The Rs. 1.5 lakh is the maximum limit.

Q9: For how many years can I claim the 80EEB deduction?

A: You can claim the deduction every year from the year the loan repayment (interest component) begins until the loan (sanctioned within the eligible period) is fully repaid.

Q10: What if I sell my electric vehicle before the loan is fully repaid?

A: To continue claiming the deduction, you generally must own the electric vehicle. If sold, the deduction for the remaining period may not be allowed.

Q11: Can I claim Section 80EEB if the loan is in my spouse's name but I am paying the EMI?

A: The deduction can typically be claimed by the individual in whose name the loan is sanctioned and who is paying the interest. The vehicle should also ideally be registered in their name.

Q12: What are the new disclosure requirements for Section 80EEB in ITR for AY 2025-26?

A: You need to provide details like vehicle registration number, lender's name and PAN, loan account number, loan sanction date, total loan amount, and outstanding loan as of March 31st in your ITR. (Refer to the section on How to Claim Section 80EEB in Your Income Tax Return (ITR) for AY 2025-26 (FY 2024-25))

Q13: Can I claim depreciation on my EV and also claim 80EEB?

A: If you use the EV for business, you can claim depreciation as a business expense. The 80EEB deduction for interest (up to Rs 1.5 lakh) is a separate claim for individuals. Interest over Rs 1.5 lakh might be claimable as a business expense if conditions are met.

Q14: What if my EV loan was sanctioned on March 31, 2023? Am I eligible?

A: Yes, if the loan was sanctioned on or before March 31, 2023, you are eligible to claim the deduction for interest paid.

Q15: Where can I find the official information about Section 80EEB?

A: You can refer to the Income Tax Act, 1961, and relevant notifications or circulars on the official Income Tax Department website.

Comments