If Taxable Income is Less than Basic Exemption Limit, Do You Need to File Returns?

- Farheen Mukadam

- Oct 15, 2024

- 7 min read

Updated: Jan 2, 2025

Filing income tax returns (ITR) is a key responsibility for individuals with taxable income. However, what happens if your income is below the basic exemption limit? Is filing a return still necessary? While you may assume that no taxes mean no filing, there are several situations where filing an ITR is required even if your income doesn't exceed the exemption threshold.

In this article, we will explore the circumstances under which you still need to file your returns, the potential benefits of filing voluntarily, and how it could impact your financial future.

Table of Contents

Understanding the Basic Exemption Limit

The basic exemption limit is an important concept in Indian income tax law. It's essentially a limit set by the government below which individuals don't have to pay any income tax. In simpler terms, it's a tax-free allowance.

The basic exemption limit isn't a fixed amount and can change from year to year, depending on the government's fiscal policy. It's usually adjusted to account for inflation and other economic factors.

The exemption limit varies based on several factors:

Residential Status: Individuals are categorized as residents, non-residents, or deemed residents based on their physical presence in India. The exemption limit is generally higher for residents compared to non-residents.

Age: Individuals aged 60 and above are eligible for a higher basic exemption limit than those below 60. Similarly, individuals aged 80 and above enjoy an even higher exemption.

Disability: Individuals with disabilities may qualify for a higher basic exemption limit, depending on the severity of their disability.

Other Deductions: There are various deductions available to reduce taxable income, such as deductions for medical expenses, home loan interest, and donations. The exemption limit effectively increases when these deductions are claimed.

What to do if Taxable Income is less than the Basic Exemption Limit?

According to Indian income tax laws, individuals are generally not obligated to file Income Tax Returns (ITRs) if their annual income is below the basic exemption limit. However, there are specific circumstances where filing an ITR becomes mandatory, even if your income falls within the exemption threshold. Let's explore these conditions:

High-Value Bank Deposits:

Savings Accounts: If your combined annual savings bank deposits across all accounts exceed Rs. 50 lakhs, you must file an ITR.

Current Accounts: A total deposit of Rs. 1 crore or more in current accounts during the financial year necessitates ITR filing.

Business Activities:

Sales Turnover: Individuals with annual sales turnover exceeding Rs. 60 lakhs are required to file ITRs.

Professional Income: If your professional income surpasses Rs. 10 lakhs, ITR filing is mandatory.

Financial Transactions:

Electricity Bills: An annual electricity bill exceeding Rs. 1 lakh triggers the requirement to file an ITR.

TDS/TCS: If the Tax Deducted at Source (TDS) or Tax Collected at Source (TCS) amounts to more than Rs. 25,000 (Rs. 50,000 for senior citizens), ITR filing is mandatory.

Foreign Assets and Transactions:

Foreign Assets: Owning foreign assets or being a beneficiary of foreign assets requires ITR filing.

Foreign Travel: Spending Rs. 2 lakhs or more on foreign travel for yourself or others during the financial year makes ITR filing mandatory.

Even if you're just an authorized signatory on a foreign bank account, you might still need to file an Income Tax Return (ITR) in India. This applies regardless of whether the assets in the account are movable (like cash or investments) or immovable (like property).

For instance, if you opened a foreign bank account while traveling abroad and forgot to close it after returning to India, you may be required to declare this account and file an ITR.

Minimum Income to File Tax Return in India

The minimum income required to file an income tax return depends upon a person’s age and chosen tax regime. Then if the gross income increases Rs. 2.5 lakhs in a financial year, you generally need to file income tax returns.

These limits are based on your gross income before deducting certain expenses and allowances specified in Sections 80C to 80U and Section 10. So, your actual taxable income might be lower after applying these deductions.

When you invest in assets like mutual funds or stocks and hold them for a specific period (usually longer than a year), any profits you make are considered long-term capital gains. The way these gains are taxed depends on the type of asset you're investing in. The Income Tax Act outlines different rules for taxing long-term capital gains from various assets.

Why should you File an ITR even if You have No Income Tax Liability?

Below are some reasons described why you should consider filing ITR even with no income tax liability-

Documentation and Record-keeping

Filing an Income Tax Return (ITR), even if you don't owe any taxes, is like keeping a financial diary. It creates a record of your income and expenses, which can be invaluable for various purposes.

Loan Applications

When applying for loans, financial institutions often require proof of income. An ITR serves as a reliable document to demonstrate your earning capacity and financial stability.

Visa Applications

Many countries require proof of income when you apply for visas. An ITR can be essential in demonstrating that you have the financial means to support yourself during your stay.

Government Benefits

Some government benefits, like scholarships or subsidies, may require you to submit proof of income. An ITR can help you qualify for these benefits.

Financial Planning

Having an ITR can be helpful for long-term financial planning. It allows you to track your income and expenses over time, identify areas where you can save or invest, and make informed decisions about your finances.

Legal Matters

In certain legal cases, an ITR can be used as evidence to prove your financial situation.

Refunds Claim

If you've already paid taxes through TDS (withheld from your income) or advance tax payments, but your total tax bill is lower than what you've paid, you might be entitled to a tax refund. To claim this refund, filing an Income Tax Return (ITR) is essential.

Here's an example: Your income before deductions might seem high enough to require taxes. However, once you factor in deductions for things like investments or home loans, your actual taxable income might fall below the minimum amount you need to pay taxes (Rs. 2,50,000 for most people). In such cases, if you've paid more tax than you owed, filing an ITR is the way to get your money back.

Losses Carry Forward

If you've lost money, for example, from selling investments, you can use that loss to

potentially reduce your taxes in the future. However, to do this, you need to file an Income Tax Return (ITR). This process is called carrying forward losses. It's like saving up your losses to offset future profits and pay less tax.

Meeting the Threshold Requirements

Even if you don't owe any income tax because your earnings are below the taxable limit, there might be specific thresholds where filing an Income Tax Return (ITR) becomes mandatory. These thresholds can differ based on your age, the kind of income you have, and whether you're a resident or non-resident of India. It's important to understand the rules that apply to you.

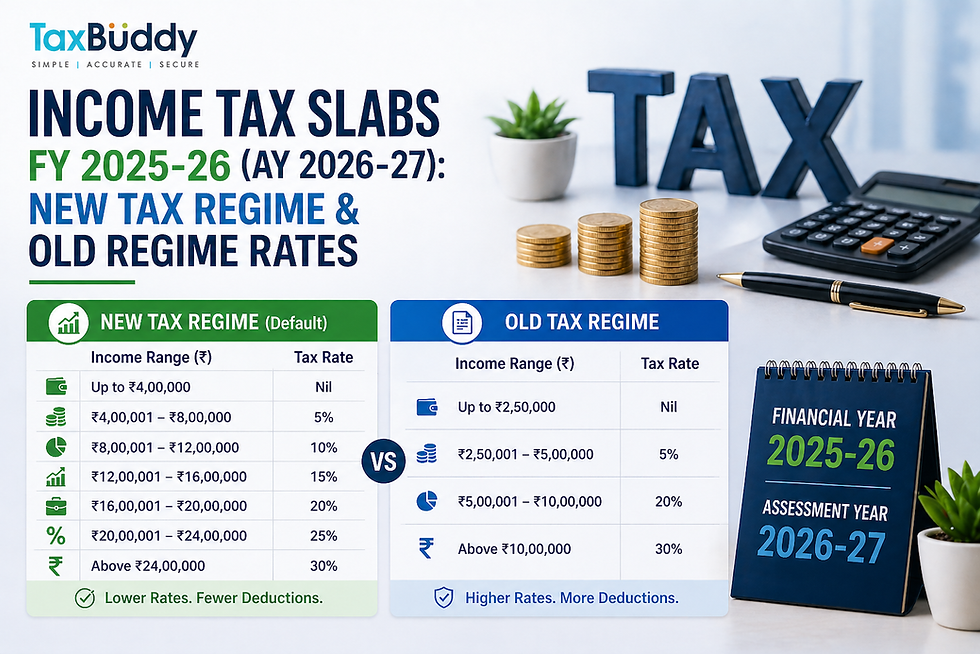

Basic Tax Exemption Limit under Old and New Tax Regimes

When filing Income Tax Returns (ITRs) for the financial year 2023-24, the basic exemption limit (the income you can earn without paying taxes) depends on your age and whether you choose the old or new tax regime:

Old Tax Regime:

Individuals under 60: The basic exemption limit is Rs. 2.5 lakhs.

Senior Citizens (60-79 years): The basic exemption limit is Rs. 3 lakhs.

Super Senior Citizens (80+ years): The basic exemption limit is Rs. 5 lakhs.

New Tax Regime:

Everyone: The basic exemption limit is Rs. 3 lakhs for all individuals, regardless of age.

Conclusion

Even if the income does not exceed the basic exemption limit, there are some benefits for filing income tax returns. It can help to get the TDS refunds and carry forward the losses to adjust the profits in the upcoming year. Ahead when you apply for a loan, the lender can ask for an ITR filing copy. The copy allows us to check the repayment capacity and the loan approval process gets faster. So, filing an income tax return every year can benefit you in the long run.

FAQs

Q1. What does the basic exemption limit mean?

The basic exemption limit is the maximum amount of income you can earn without having to pay income tax.

Q2. What is the benefit of the basic exemption limit?

The basic exemption limit is great because it means you don't have to pay income tax if your earnings are below that amount. It's a helpful rule set by the Indian government.

Q3. What are the benefits of filing an ITR?

Filing ITR ensures compliance with the tax laws. It facilitates tax refunds and allows losses to carry forward, helps avoid default notices and keeps you updated with tax regulations.

Q4. What is the basic exemption limit to file an ITR?

The basic exemption limit for people of 60 years of age is Rs. 2.5 lakhs gross income within a financial year. And 3 lakhs under the new regime.

Q5. Are there any penalties for not filing an ITR when I have no tax liability?

Even if you don't owe any taxes, not filing your required tax returns can get you into trouble. Many places have rules that say you have to file, no matter what. Failing to do so could result in fines or other legal problems. So, it's important to follow the tax laws and file the necessary returns to stay out of trouble.

Q6. What is an exempted income?

Exempted income refers to the income that is not taxable. There are rules and regulations that are different from country to country.

Q7. Should I file an ITR if my income is below the basic exemption limit of Rs 5 lakh?

Even if you earn less than Rs. 5 lakhs and get a tax break of Rs. 12,500 (Section 87A), you still need to file an Income Tax Return (ITR) for the financial year 2023-24. This is because the basic exemption limit is Rs. 2.5 lakhs, and if your income is above that amount, you must file an ITR, regardless of any tax breaks you might get.

Q8. What is the basic exemption limit in the new tax regime?

For the financial year 2023-24, the basic exemption limit was raised to Rs. 3 lakhs from the previous amount of Rs. 2.5 lakhs if you're using the new tax regime. This means you can earn up to Rs. 3 lakhs without having to pay income tax.

Q9. What are the factors that determine the basic exemption limit?

The factors that check basic exemption limits are residential status, age, and disability.

Q10. What is the minimum income for ITR?

Generally, if your income exceeds Rs. 2,50,000, you're required to file an Income Tax Return (ITR). However, there are some situations where this might not be the case. For example, if you're a senior citizen or have certain deductions, the rules might be different.

Comments